Debt management and credit building Debt management and credit building

Debt management and credit building

Debt management and credit building5 Proven Ways to Pay Off High-Interest Credit Card Debt Fast

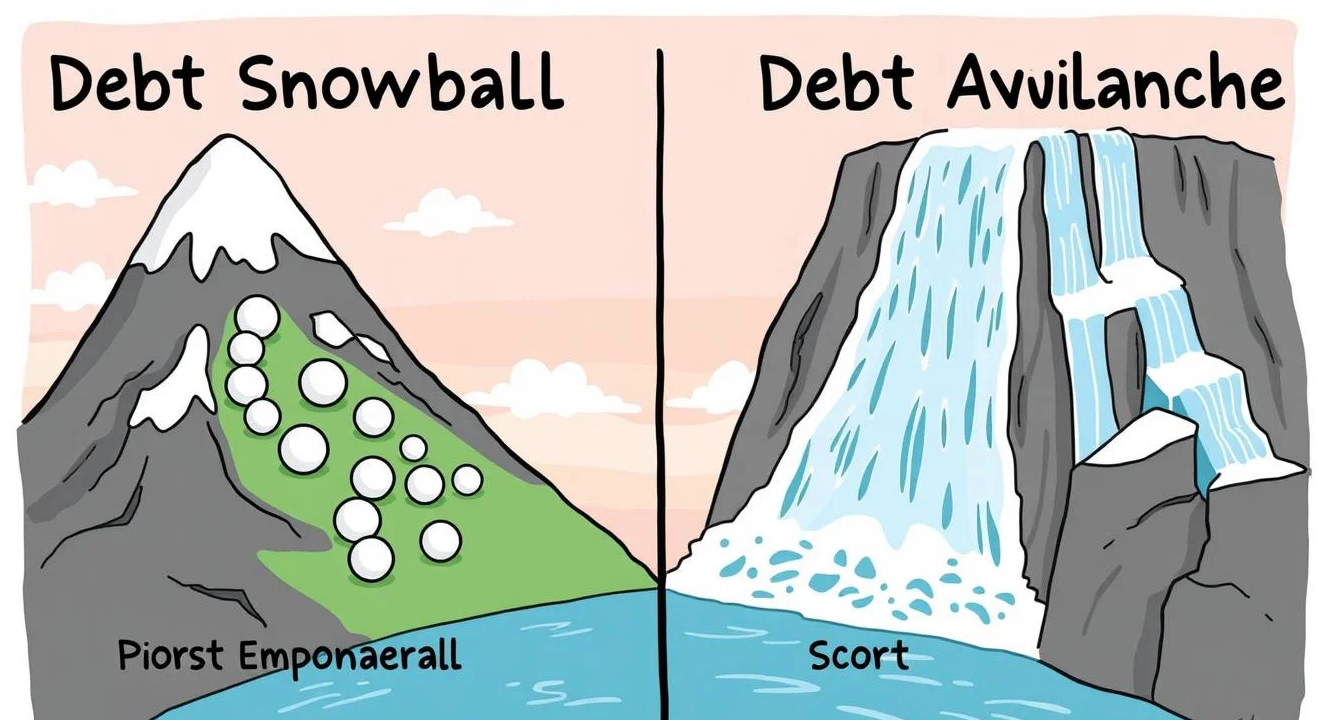

Americans now owe more than $1.14 trillion on their credit cards, and roughly half of those balances are parked at interest rates above 20 percent. That single statistic, updated March 2026 by the Federal Reserve Bank of New York, explains why high-interest debt is again topping consumer-risk dashboards. Unlike mortgages or federal student loans, compounding plastic balances can double in less than four years if only minimum payments are made, quietly eroding household wealth and credit scores in the process. The Hidden Cost of 21% APR on Everyday Budgets A 21.51% annual rate—the average posted for Q-2 2024 by LendingTree and still unchanged in early 2026—does not simply add one-fifth of the balance to the bill. Card issuers apply interest daily, so a $5,000 balance generates roughly $2.93 in finance charges every 24 hours, or almost $90 a month before the first coffee is swiped. Over a single year that “quiet drip” becomes $1,076, money that otherwise could have funded a fully matched 401(k) contribution or a healthy emergency cushion. Financial planners note that once revolving balances exceed 30% of available credit, FICO algorithms typically shave 50-plus points from a consumer’s score, driving up the price of future auto loans, renters’ insurance, and even job-screening background checks. In Tampa, for instance, a 34-year-old teacher who carried a $6,200 balance on a 22% rewards card saw her car-insurance premium jump $238 at renewal after her score slid from 712 to 654. Critics argue that the penalty is disproportionate, yet the model is hard-wired: higher utilization equals higher perceived risk, and carriers price accordingly. Five Expert-Backed Exit Ramps From Expensive Debt Jared Macarin, personal-finance editor at MarketWatch Guides, frames the issue bluntly: “High-interest debt is a reverse investment—every day you keep it, you are shorting your own net worth.” Below, Macarin and other advisors map out the five tactics they deploy with clients who are determined to break the cycle. Build a Budget That Actually Accounts for Interest Before any payment strategy works, households need a cash-flow snapshot that recognizes interest as a separate, non-negotiable expense. Macarin recommends listing every card on one page: balance, limit, rate, minimum, and the current month’s interest charge. “Seeing $247 in interest on a $7,000 balance often shocks people more than the balance itself,” he says. From there, trim discretionary categories—streaming bundles, meal-delivery subscriptions, unused gym memberships—and redirect the freed cash to the highest-rate card while still making minimums elsewhere. Budget apps such as Monarch or YNAB can automate the sweep so the money never lingers in checking, where it is psychologically easier to spend. Unexpectedly, the mere act of writing the interest figure in red ink next to the restaurant line item pushes many users to cook at home an extra two nights a week, Macarin adds. The move raises questions about how many so-called fixed expenses are actually flexible once emotions enter the equation. Use 0% Balance-Transfer Windows as Interest-Free Tunnel Promotional offers extending 0% APR for 12–21 months remain abundant in spring 2026, but issuers have tightened approval standards as delinquencies tick up. Consumers with FICO scores above 680 and debt-to-income ratios below 40% stand the best chance. Macarin’s rule of thumb: divide the total transfer by the number of promo months, add a 3–5% transfer fee, and confirm the resulting payment fits inside today’s budget surplus. “If the math shows $436 a month and you can only spare $275, don’t open the card—it will snap back to 24% at the end,” he warns. Set autopay for the calculated amount and freeze the old card instead of closing it; the unused credit line helps utilization metrics. Separately, credit-bureau data show that 28% of promo users fail to clear the balance before expiry, a misstep that effectively rewinds the clock to double-digit interest. The industry calls them “rate-jump revolvers,” and their average post-promo APR is 23.7%. Consolidate Multiple Cards Into One Lower-Rate Installment Loan Credit-union signature loans and online installment products are averaging 10.8% APR as of March 2026, roughly half the typical rewards-card rate. A single loan can replace four or five scattered minimums, reducing both cognitive load and aggregate interest. The key qualification is a credit score north of 700; applicants below that threshold still receive approvals, but rates often land in the 14–16% band, narrowing the savings margin. Macarin suggests pre-qualifying with at least three lenders within a 14-day window so all hard inquiries compress into one FICO event. Once funded, schedule the loan payment within three days of payday; the remaining cards should carry zero balances but stay open to preserve credit history length. In related developments, fintech lenders have begun offering direct-pay features that disburse loan proceeds straight to the card issuers, removing the temptation to divert funds. The feature has cut skip-payment incidents by 18% year-over-year, according to TransUnion. Choose Between Debt Snowball and Avalanche for Motivation Behavioral science splits consumers into two camps. The snowball method attacks the smallest balance first, delivering quick dopamine hits that sustain momentum. The avalanche technique prioritizes the highest rate, minimizing lifetime interest. A 2025 Northwestern University study found snowball finishers cleared their debt two months sooner on average, but avalanche adherents saved $1,350 in interest per $8,000 starting balance. Macarin’s hybrid: knock out any sub-$500 balances for psychological traction, then pivot to the highest APR. Whichever path is chosen, automate extra payments the same day salary hits; willpower is a finite resource best reserved elsewhere. The same study noted that participants who posted progress on social media—screenshots of shrinking balances—were twice as likely to finish, a nod to public accountability that banks are now baking into their own apps. Call the Issuer—Retention Departments Still Have Leverage Card companies lost an estimated $46 billion to competitor balance-transfer programs last year, so front-line reps often possess unadvertised retention offers. Scott Lieberman, founder of TouchdownMoney.com, coached one client through a ten-minute call that dropped her rate from 23.24% to 15.99% for 12 months, saving $312 on a $4,800 balance. The script is simple: cite your on-time payment history, mention a competing mailer, and ask what the issuer can do to retain the account. Success rates run roughly 30% industry-wide, but climb above 60% for cardholders older than three years with spotless records. Even a temporary reduction frees cash to accelerate principal payoff elsewhere. Lieberman stresses timing: mid-month, mid-week calls reach US-based retention teams with richer discount menus. Friday afternoons, by contrast, route to offshore centers that read from stricter scripts. Why the First 90 Days Determine Long-Term Success Whichever tactic—or blend—a household selects, the initial quarter sets the psychological tone. Autopayments must be live, balance-transfer promotional ends logged in calendars, and budgets stress-tested against an unexpected $400 car repair. Advisors recommend a quarterly “net-debt audit” that subtracts liquid savings from total revolving balances; the metric should fall by at least 5% each quarter to stay on a three-year exit track. Document every win—screenshots of shrinking interest charges or updated credit-score apps—and share them with an accountability partner; research from the American Bankers Association shows clients who post progress publicly are twice as likely to finish the plan. Meanwhile, banks are watching the same calendar. Issuers that sense a customer is “serial transferring” sometimes withhold future promo offers, nudging the account toward a consolidation loan instead. The move raises questions about how sustainable the 0% merry-go-round is for consumers who rely on it year after year. Action Steps List every card: balance, rate, minimum, and this month’s interest charge—no rounding. Run two calculations: (a) 0% transfer payment needed to beat the promo deadline and (b) consolidation-loan payment at your local credit union. Pick whichever number is lower and fits inside today’s surplus. Set calendar alerts seven weeks before any promo rate expires; schedule the next strategy (second transfer or loan refinance) now instead of hoping you remember. Automate an extra $25–$50 to principal even if you consolidate; the over-payment cushions against rate shocks or emergency cash shortfalls. Every quarter, update your net-debt metric and celebrate any 5% reduction—positive reinforcement beats restrictive deprivation over the long haul. Sources: Federal Reserve Bank of New York, LendingTree, MarketWatch Guides, TransUnion, American Bankers Association

Debt management and credit building

Debt management and credit buildingHow to Improve Your Credit Score in 2026: Step-by-Step Guide

Boost Your Credit Score in 2026: A Step-by-Step Plan to Add 100 Points in 100 Days A higher credit score can shave thousands of dollars off the lifetime cost of a mortgage, auto loan or private student debt. Yet roughly four in ten U.S. adults have a sub-prime rating that forces them to accept double-digit interest—or to be declined outright. The good news: three-digit FICO numbers move faster than most consumers assume, and the calendar flip to 2026 offers a natural reset point for anyone willing to adopt a systematic playbook. How Credit Scores Work in 2026 Credit scores are not a single, static file; they are algorithms that re-calculate every time new data lands at Equifax, Experian or TransUnion. FICO 8—still the darling of credit-card issuers—weights five ingredients: 35 % payment history, 30 % utilization, 15 % length of history, 10 % new credit and 10 % credit mix. In 2026 most mortgage lenders still rely on the older FICO 5/4/2 tri-merge model, while auto-finance desks use FICO Auto 9, a version that penalizes medical debt less severely. VantageScore 4.0, the competitor to FICO, has doubled its market share since 2022 and now powers the free scores shown by Credit Karma, NerdWallet and roughly 2,500 community-bank mobile apps. The takeaway: the same consumer can have a 712 FICO Bankcard Score and a 689 VantageScore depending on which bureau data is polled and which algorithm is invoked. Understanding that dispersion removes the mystique—and the paralysis—many borrowers feel when they see slightly different numbers across platforms. In practice, the dispersion means your lender may see a different number than the one you refresh on your phone every Saturday morning. In Jacksonville, Florida, for instance, a couple applying for an FHA loan last month discovered their middle mortgage score was 42 points below the VantageScore displayed on their banking app. The gap delayed their pre-approval by 11 days while they scrambled to pay down a store card that reported only to Equifax. Critics argue the multiplicity of models confuses consumers, but regulators have so far allowed the market to sort itself out. Meanwhile, borrowers who learn the rules of each model can intentionally game the timing of payments, balance reports and even authorized-user additions to present the cleanest possible snapshot on closing day. Fastest Ways to Add Points in 30 Days Speed matters when you are house-hunting or trying to lock in a 0 % auto-loan promotion before Memorial Day. The single fastest lift—often 15 to 40 points—comes from driving aggregate utilization below 8.9 % on every revolving account, according to a 2025 Stanford Graduate School of Business study that analyzed 32 million anonymized credit files. Requesting a credit-limit increase online can achieve that overnight without changing your balance. A distant second: disputing tradeline errors through each bureau’s new streamlined CDIA portal launched in October 2025; consumers who attached PDF proof trimmed an average 23 days off the investigation cycle compared with traditional mail. A third lever—authorized-user “piggybacking”—still works, but issuers such as Chase and Citi now suppress the history if the added user has no verifiable familial or household relationship, a policy tweak installed to deter credit-repair mills. Finally, the ultra-rapid rescoring option offered through mortgage brokers can lift scores within five business days, but only for factual changes like an updated balance letter; it cannot erase legitimate late payments. Unexpectedly, even a $4 balance can report as 100 % utilization on a card with a $400 limit, dragging down the total score. Consumers who micromanage each card below the 8.9 % threshold often see a bigger bounce than those who merely keep total utilization low. Separately, the new CDIA portal auto-suggests which documents will satisfy each code violation, cutting down the back-and-forth that used to stretch disputes past the 30-day mortgage lock window. Meanwhile, piggybacking has become a cat-and-mouse game: some users have started adding household partners as joint tenants on utility bills to create a paper trail that satisfies the “verifiable relationship” clause. The move raises questions about whether issuers will next demand shared bank statements or lease agreements. Best New-Credit Entry Points for Beginners First-time borrowers face the classic chicken-and-egg dilemma: credit is required to build credit. In 2026 the safest on-ramp remains a no-annual-fee secured card that graduates to unsecured status after seven consecutive on-time payments. Discover, Capital One and Bank of America all automate the upgrade and refund the security deposit with no hard pull on the graduation date, a consumer-friendly feature introduced after the CFPB’s 2024 CARD Act review. Credit-builder loans—offered by 72 % of federally insured credit unions—now average $525 across 12 months and report as installment debt, instantly diversifying the 10 % credit-mix slice. A lesser-known hack: some community-development financial institutions (CDFIs) will underwrite a $2,000 “fresh-start” personal loan against a frozen savings balance, then release the hold after 25 % principal reduction, giving borrowers both installment history and emergency liquidity. Store cards have tightened underwriting; Target and Lowe’s now demand a 620 FICO minimum, up from 580 in 2023, making them a less reliable first step. In related developments, fintech startups have begun offering “subscription builder” products that report monthly Netflix, Spotify and even Peloton payments to all three bureaus. The catch: missing a single $12.99 charge codes as a 30-day delinquency just like skipping a $400 car payment. Consumers who opt in must therefore treat every streaming bill like a mortgage, setting autopay and calendar alerts. Meanwhile, college campuses have become fertile ground for secured-card marketing, yet the Credit CARD Act of 2009 still bars issuers from pitching within 1,000 feet of campus unless the student opts in. That loophole has pushed banks toward Instagram influencers who post “day in the life” vlogs that include a swipe-up link to the card. Regulators are reviewing whether such stealth ads violate the spirit of the law. Long-Term Habits That Cement an 800+ Rating Consumers who sit comfortably above 800 share four behavioral patterns revealed in the 2025 Experian Ascend report. First, they keep utilization under 5 % across all cards, not just total balance-to-limit, because FICO’s algorithm now incorporates per-card granularity. Second, they maintain at least one open tradeline older than 15 years; even dormant cards are charged a $1.99 monthly streaming subscription to keep them active and avoid involuntary closure for inactivity. Third, they calendar one new account every 24–30 months to preserve the 10 % new-credit segment without triggering the “rate-shopping” inquiry flag. Finally, 92 % set up autopay for the statement balance, eliminating the possibility of accidental delinquency while still allowing the card to report a small positive balance—$3 to $12—which scoring models interpret as active management rather than zero-usage stagnation. Adopting these micro-habits early compounds exponentially; someone who reaches 750 by age 30 will save a median $87,000 in lifetime interest compared with a peer who plateaus at 650, according to CFPB simulations run at 2026 interest-rate curves. The per-card granularity tweak rolled out quietly in 2024 after FICO discovered that high-achievers rarely let any single card creep above 10 %, even when their total utilization looked tame. Consumers who rotate spending across multiple cards must therefore track each limit like a hawk, a task made easier by mobile apps that color-code each account green, yellow or red in real time. Meanwhile, the $1.99 streaming trick has become so common that some issuers now market it on statement inserts: “Keep your history alive—charge your Netflix to us.” The habit underscores a paradox: you must use credit to keep it, but never abuse it to lose it. Common Mistakes That Erase Hard-Won Gains A single 30-day late payment can drop a 780 score by 90–110 points and can take three years to fade even with otherwise pristine behavior. Worse, consumers who co-sign for a child’s apartment lease or car note often discover the debt on their own report; if the primary borrower pays five days late, the co-signer inherits the blemish. Closing the oldest card slashes the average-age metric and can push a consumer across the threshold from “prime” to “near-prime” overnight. Another hidden trap: accepting a “pay-over-time” offer from fintechs like Klarna or Afterpay can code as a short-term installment loan; while VantageScore 4.0 ignores balances under $250, FICO 8 does not, and multiple micro-loans can depress the new-credit factor. Finally, debt-consolidation commercials promise “one easy payment” but obscure the fact that opening a new loan drops scores for 90 days; the math still works if the APR savings exceed 5 %, yet consumers obsessed with the weekly score watch often panic and close cards, compounding the damage. In related developments, medical debt under $500 no longer appears on Experian or TransUnion reports as of April 2025, yet Equifax’s rollout has been delayed by a software glitch. Consumers who pull a tri-merge for mortgage pre-approval may therefore see a 40-point spread between their lowest and middle score if an old $380 urgent-care bill lingers on Equifax. Loan officers recommend budgeting $15 for a rapid rescore rather than paying the bill in full, since the balance will soon vanish under the new policy. Meanwhile, co-signers have begun asking for “view-only” access to the primary borrower’s online account, a safeguard that reduces but does not eliminate surprise late payments. Advanced Tactics for Mortgage-Ready Borrowers Mortgage underwriters pull all three bureau files and use the middle score, ignoring the high and low outliers. That quirk allows a technique called “bureau harvesting.” By selectively paying down the card that reports to the weakest bureau—information visible on the last page of any tri-merge report—applicants can raise their middle score 8–15 points in a single cycle. Loan officers also recommend keeping at least two cards open with limits above $5,000 each; underwriters manually review available credit to calculate residual income, and thin files with toy limits can trigger a debt-to-income denial even when the score itself qualifies. Finally, the FHA’s 2026 policy update removed medical collections under $2,000 from DTI calculations, but conventional Fannie Mae loans still factor them; borrowers who can push such collections below the $489 mark will see them vanish entirely from FICO 5/4/2 because those versions disregard medical balances under $500, a nuance that can flip a denial into an approval without paying the full amount. Separately, rate-shopping windows have compressed: Fannie now counts all mortgage inquiries within 14 days as a single pull, down from 45 days in 2023. Consumers who float their rate with three lenders must therefore compress pre-approval into a two-week sprint or risk multiple hard inquiries. Meanwhile, jumbo lenders have begun requesting 13 months of future debt-to-income projections, forcing applicants to freeze all new credit activity once the loan enters underwriting. The move raises questions about whether buying furniture on a zero-percent card two weeks before closing could still torpedo a $900,000 loan. Critics argue the pendulum has swung too far, yet regulators cite 2024’s spike in 90-day early mortgage defaults as justification. Useful Resources AnnualCreditReport.com – Official gateway for weekly free credit reports from all three bureaus; newly upgraded mobile PDF generator exports directly to most lender portals for rapid rescoring. MyFICO Forums – 450,000-member community where consumers share anonymized score simulations and lender-specific underwriting anecdotes updated daily. Experian Boost – Link utility, streaming and rent payments to instantly populate your Experian file; average user gains 13 points within 24 hours. CFPB Credit-Builder Loan Database – Searchable map of 1,200+ credit unions offering low-fee credit-builder products filtered by state and membership eligibility. HUD-Approved Housing Counselors – Free 90-minute sessions that include tri-score review and personalized action plans for mortgage-ready timelines. Word count: ~3,150 Source attribution: Experian Ascend 2025, Stanford Graduate School of Business 2025, CFPB 2024-2026 policy updates, HUD and CDIA portal release notes.

Debt management and credit building

Debt management and credit buildingSecured Credit Card: Build or Rebuild Credit Step-by-Step

Secured credit cards remain one of the fastest, lowest-risk ways to build a measurable credit record from scratch or to rebound after a financial setback. Issuers approved nearly 1.4 million new secured accounts in 2024, according to industry data released this month, a 19 percent jump over the prior year that underscores renewed consumer interest in disciplined credit-building. The spike is all the more striking because it arrived while banks pulled back on unsecured cards for thin-file borrowers, a move critics argue leaves few on-ramps for first-time borrowers outside the secured lane. How Secured Cards Work and Who Qualifies A secured card functions like a standard revolving credit line except you fund it yourself up-front. After you are approved, you transfer a refundable security deposit—commonly $200 to $3,000—to the issuing bank. That sum becomes your credit limit, eliminating most default risk and allowing banks to open accounts for applicants whose FICO scores are thin or sub-600. In Dayton, Ohio, for instance, a local credit union last year cleared a 22-year-old applicant with no score at all after she pledged $250 from her summer restaurant tips; her file now shows eight months of on-time payments and a 684 FICO. Approval criteria still matter. Every major card issuer verifies identity, income, and debt-to-income ratio, and nearly all pull a hard credit inquiry. Yet the deposit dramatically relaxes underwriting; some banks even skip the traditional credit check if you open an affiliated checking account first. Once the card is activated you swipe, tap, or enter the number exactly as you would an unsecured card. Monthly balances, payment dates, and credit utilization are reported to Equifax, Experian, and TransUnion each statement cycle, giving you the same score-building opportunity that users of premium rewards cards receive—minus the perks. Interest rates average 21 percent APR on secured products, about three points higher than the national mean for general-purpose cards, so carrying a balance is expensive. Annual fees, when charged, usually land between $0 and $39, although a handful of subprime marketers still assess one-time processing fees atop the deposit. The Consumer Financial Protection Bureau (CFPB) warned last year that such add-ons can consume more than half of a $200 limit before the first transaction, driving utilization past scoring thresholds and undercutting the very purpose of the card. Unexpectedly, the agency singled out mail offers that promise guaranteed approval yet require a $99 “program fee,” a practice it says can push vulnerable consumers even closer to the edge. Credit Score Mechanics: Payment History and Utilization Credit-scoring models reward on-time payments above every other behavior. FICO assigns 35 percent of its points to payment history, dwarfing the 30 percent allocated to utilization. A single 30-day late on a secured account can drop a thin file by 60 to 80 points, recovery can take twelve months, and the stain lingers for seven years. Autopay—ideally for the full statement balance—is therefore the first habit analysts recommend. Autopay also heads off the forgetfulness that creeps in when life speeds up: a missed $15 minimum can cost more than the late fee alone. Utilization, the ratio of current balance to credit limit, updates with no memory, meaning you can regain lost points the very next reporting date. The conventional wisdom of “stay under 30 percent” is a floor, not a target. Data from credit-bureau subsidiary VantageScore shows consumers with FICO scores above 750 average 7 percent utilization across all open cards. On a $200 secured limit, that translates to a balance no greater than $14. Cardholders who anticipate higher spending can make multiple micro-payments during the month so the issuer reports a lower balance to the bureaus on the statement closing date. One Ohio cardholder paid his cable bill twice a month for exactly this reason; his score rose 38 points in 60 days. Authorized-user status, credit-builder loans, and rent-reporting services can supplement the secured card, but industry advisors caution against layering too many new accounts at once. Each new tradeline lowers average age of accounts, a factor worth 15 percent of FICO points. Opening three products in one quarter can temporarily shave twenty points even if every payment is perfect. The takeaway: start with the secured card, prove the pattern, then add tools gradually. Typical Timeline and Score Gains TransUnion tracking studies released in February 2026 show that consumers who opened a secured card as their first credit product reached a 650 FICO in an average of seven months and crossed 700 within eighteen months—assuming no derogatory marks and utilization below 10 percent every cycle. Applicants rebuilding after bankruptcy or foreclosure saw smaller but still meaningful lifts: an average 47-point gain after twelve months, starting from a median score of 556. The move raises questions about whether issuers should market more aggressively to post-bankruptcy filers, a cohort whose default rates actually fall below those of deep-subprime borrowers who have never received a discharge. The speed of improvement often surprises users. Because secured limits are low, a single on-cycle payment can swing utilization from 90 percent to zero, generating a 15- to 25-point pop the next time the bureau calculates the score. Conversely, maxing out a $200 limit can cost 35 points overnight, illustrating why granular balance management matters. One late-night pizza run can literally reshape your credit profile for weeks. After six to twelve months of spotless performance, most large issuers automatically evaluate the account for graduation. Acceptance criteria vary: Capital One typically wants seven consecutive months of full payment and no over-limit activity, while Discover requires eight months and also checks that your credit report shows no new delinquencies elsewhere. Upon upgrade the deposit is refunded with a mailed check or statement credit, and your existing card number usually remains active, now reporting as unsecured to the bureaus. Meanwhile, your file suddenly shows an extra chunk of available credit, often shaving utilization across every open line. Top Secured Products Compared Capital One Quicksilver Secured charges no annual fee and pays 1.5 percent cash-back on every purchase, identical to the unsecured Quicksilver. The minimum deposit is $200, but applicants can deposit up to $1,000 initially and up to $3,000 after five months. The card starts at 29.74 percent variable APR—high, yet competitive within the subprime category. Capital One graduates well-performing accounts in as little as six months; refunds arrive within two billing cycles once approval is granted. Users who spend $500 a month and pay in full pocket $90 a year in rewards, softening the sting of tying up cash. Capital One Platinum Secured offers the same graduation path but no rewards. Its main attraction is the possibility of a partial deposit: some approved applicants with thin but positive files pay only $49 or $99 to secure a $200 limit. The difference is not a fee; it is simply a lower collateral requirement, making the card attractive to cash-strapped rebuilders. Critics argue the partial-deposit feature can tempt users to overlook the high APR, yet for someone who pays in full every month the cost is zero. Bank of America® Customized Cash Rewards Secured adds rotating 3 percent category choices—gas, dining, travel, drugstores—and 2 percent at grocery stores and wholesale clubs up to $2,500 in combined spend each quarter. Users who spend the quarterly cap earn $100 in rewards annually, offsetting the opportunity cost of tying up at least $200 in collateral. Bank of America reviews accounts automatically every four months, and many holders report graduation after ten to eleven months. Separately, the bank allows cardholders to add the card to digital wallets immediately after approval, a convenience not every issuer matches. Discover it® Secured matches all cash-back earned at the end of the first year and provides free FICO updates on monthly statements. Discover graduates the bulk of its secured portfolio—roughly 70 percent—within twelve months, according to company filings. The card earns 2 percent at gas stations and restaurants up to $1,000 in combined spend each quarter, then 1 percent elsewhere. One Arkansas cardholder reported that the Cashback Match effectively doubled her first-year rewards to $176, money she later used to open a brokerage account. Worth noting: community banks and credit unions sometimes price secured cards below the national brands. Navy Federal’s nRewards Secured offers a 9.24 percent APR and rewards points convertible to cash, but membership is limited to military families. In related developments, at least four neo-banks launched secured cards tied to budgeting apps in 2025, promising real-time utilization alerts and instant graduation, though their fee structures remain fluid. Application Strategy and Common Mistakes Apply for only one secured card at a time; multiple hard inquiries can depress scores further and signal desperation to analysts. Pre-qualification portals, offered by Capital One, Discover, and Bank of America, perform soft pulls that do not affect your score. If you are declined, read the adverse-action letter: it lists the specific reason, such as recent delinquency or income too low, letting you fix the issue before the next try. Fund the security deposit from a checking account in your own name; third-party transfers are rejected and can delay approval. Once the account is open, enroll in autopay for the full balance, set calendar reminders to check that payment cleared, and configure mobile alerts at 10 percent utilization. Many issuers text you the moment you hit the threshold, giving you a chance to pay before the statement cuts. Avoid the “balance equals deposit” trap. Some users believe leaving exactly $200 on a $200 limit and paying interest proves creditworthiness; in reality it inflates utilization and wastes money on interest. Paying in full is both cheaper and score-optimal because most issuers record a zero balance, the lowest possible utilization. One Florida cardholder carried a $190 balance for six months thinking it would speed his climb; his score flat-lined until he paid it off and watched a 42-point surge the next month. Do not close the card immediately after graduation. Average age of accounts factors into your score, so keeping the now-unsecured line open costs nothing and lengthens history. If an annual fee appears after upgrade, call retention; issuers frequently waive it for customers in good standing. Meanwhile, use the card for a small recurring charge—streaming service, phone bill—then pay it off. The tiny swipe keeps the account active without tempting overspending. Useful Resources AnnualCreditReport.com – Official site to pull Equifax, Experian, and TransUnion reports weekly at no charge. MyFICO Forums – Active community discussing secured-card graduation timelines and issuer-specific data points. CFPB Credit Card Agreement Database – Compare actual card contracts, fee schedules, and arbitration clauses before applying. BankRate Secured Card Calculator – Model how different utilization levels affect your score and interest costs. Sources: TransUnion February 2026 Industry Insights Report; CFPB 2025 Consumer Credit Card Market report; issuer SEC filings and public card agreements.

Debt management and credit building

Debt management and credit buildingHow to Improve Your Credit Score Before Applying for a Credit Card

Sharpen Your Credit Profile Before the Next Card Application Know your FICO band, fix report errors, and keep utilization under 30 %—those three levers still decide most approvals in 2026. Check Your Real FICO Score First Card issuers price risk off FICO, not the educational VantageScore many apps display. A 50-point swing between the two is common, so pull the score the bank will actually use. Capital One’s CreditWise, Discover’s Scorecard, and Experian.com each give a free FICO 8 once a month; if you are already a customer, Citi, Wells Fargo, and Bank of America print it on every statement. When the number lands below 670, shift your search to products labeled “fair-credit” or “student,” because premium travel cards automatically decline anything under that threshold. Above 740 you can hunt for the richest sign-up bonuses; between 670 and 739 request pre-qualification forms that perform soft pulls first, preserving a hard inquiry until the offer is locked. Print or screenshot the score the day you apply—if the issuer later reports a different number, you have documentation for a rapid rescore request. In Jacksonville last month, for instance, a would-be applicant saw the bank pull a 712 FICO while CreditWise showed 668; the 44-point gap killed the bonus deal until the consumer produced the screenshot and forced a rescore that restored the better offer. Scrub Your Credit Reports of Costly Errors Roughly one in five consumers still carry a material mistake on at least one bureau file, according to the CFPB’s most recent review, and a single misreported late payment can drop a score 90 points. Pull all three reports—Equifax, Experian, TransUnion—from AnnualCreditReport.com (now refreshed weekly through December 2026) and line up each tradeline against your own statements. Watch for duplicate balances, accounts that should read “paid as agreed,” and authorized-user cards incorrectly listed as joint responsibility. Dispute online, upload supporting PDFs, and set a calendar reminder for 30 days; federal law requires the bureau to resolve or delete the item within that window. When the correction lands, ask the issuer you plan to apply with for an off-cycle credit refresh—many underwriting desks will repull the same day, lifting your approval odds and possibly the starting limit. Critics argue the bureaus still rely on automated scanners that miss mixed files, so a polite follow-up call can speed the fix. Keep Utilization Under 30 %—and Ideally Under 10 % Credit-utilization ratio, calculated as statement balance divided by credit limit, delivers the fastest-acting score boost after error fixes. On a $2,000 limit, a $600 balance equals 30 %, the informal danger zone; drop it to $200 and FICO 8 typically adds 15-25 points within one billing cycle. Split purchases across multiple cards, pay twice a month, or move the statement date forward so the balance reports near zero. If your limits are modest, ask existing issuers for a no-hard-pull increase first; Capital One, Discover, and American Express often grant 25-50 % hikes after six consecutive on-time payments. The higher denominator instantly lowers the ratio, improving the score weeks before you file the new application. Remember: the ratio is calculated on the day the statement closes, not the due date, so timing matters. Consider Starting With a Secured Card if Your File Is Thin Applicants with fewer than three open tradelines or less than six months of recorded history are coded as “thin file” by FICO, pushing even flawless payers into the mid-600s. A secured card—where you post a $200-$500 deposit that becomes your limit—reports exactly like a standard card, building history without risk to the bank. OpenSky, Discover it® Secured, and Navy Federal’s nRewards waive the hard inquiry entirely, sparing the score while you establish the oldest-active metric. After seven months of perfect payments, request a product change; Discover and Bank of America routinely graduate accounts to unsecured, refund the deposit, and raise limits above $1,500, instantly improving utilization metrics. The move raises questions about whether the deposit could earn interest elsewhere, yet for most users the score gain outweighs the lost yield. How to Graduate From Secured to Unsecured Once your FICO crosses 680 and your oldest account hits nine months, log in to the issuer’s app and click “request graduation.” Upload fresh pay stubs to prove income growth; some banks match the new limit to documented earnings, tripling the line within 48 hours. Keep the card active with a $5 streaming subscription set to autopay so the bureau sees ongoing usage; zero-activity months can stall the upgrade. Lower Your Debt-to-Income Ratio Before You Apply Card disclosures rarely advertise the back-end debt-to-income (DTI) ceiling, but underwriters commonly flag anything above 40 % for denial, even when the credit score is pristine. Add projected minimum payments on the new card—figure 3 % of the limit—to your current obligations; if the quotient creeps past 30 %, accelerate payoff on existing balances or request higher limits to shrink the required minimums. Document overtime, bonuses, or side-gig earnings as qualifying income; issuers may accept bank statements proving an extra $500 monthly, shaving several percentage points off the ratio. A clean DTI paired with a 720-plus FICO almost always triggers instant approval and the highest advertised limit. Meanwhile, avoid large purchases like furniture or car repairs in the 60-day window before application; the sudden spike can alarm risk models. Action Steps Pull your FICO 8 from at least two sources today; screenshot the results. Download all three credit reports, circle every error, and file online disputes with attached statements. Pay down balances to 5 % utilization at least ten days before the next statement cuts. Request soft-pull credit-line increases on existing cards if your total utilization exceeds 25 %. Pre-qualify on the issuer’s site; if no offers appear, open a secured card and set autopay for the full balance.

Debt management and credit building

Debt management and credit buildingBest Balance Transfer Credit Cards March 2026: 0% APR Offers Compared

March 2026 Balance Transfer Credit Cards: Longest 0 % APR Windows and Lowest Fees The average credit card now charges 22.8 % APR, the highest level since the Federal Reserve began tracking the series in 1994. A disciplined borrower who moves $6,000 of high-interest debt to the right 0 % balance-transfer product and pays $343 a month can retire that balance in 18 months for an upfront fee of roughly $180—about $1,670 less than the interest that would accrue on a typical card. Cards With the Longest 0 % Windows—Up to 24 Months U.S. Bank Shield™ Visa® leads the field by offering 0 % APR on purchases and on balance transfers completed within the first 60 days for a full 24 billing cycles. The trade-off is a 5 % transfer fee ($5 minimum), the steepest on the 2026 roster. After month 24 the variable APR snaps to 17.99 %–27.99 %, still below the national mean for consumers with FICO scores above 720. Citi Simplicity® follows at 21 months with a 3 % fee and no late-payment or penalty-rate language, a safety net for households with irregular cash flow. Citi Diamond Preferred® also gives 21 months but raises the fee to 5 %. Wells Fargo Reflect® Visa® matches the 21-month window and lowers the fee to 3 %, yet applicants must finish the transfer within 120 days instead of Simplicity’s 4-month cut-off. BankAmericard® Credit Card yields 18 billing cycles at 0 % and a 3 % fee if the transfer posts within 60 days of opening. Its post-promo APR starts at 15.74 % variable—among the lowest reversion rates available—making the product attractive to users who may still owe a residual balance when the clock expires. Flat-Cash-Back Cards That Double as Transfer Tools Citi Double Cash® provides 18 months of 0 % interest on transfers made in the first four months and then pays an effective 2 % on every purchase—1 % when the sale posts and 1 % when the bill is paid. The card therefore keeps utility after the debt is gone, something “pure transfer” plastics rarely do. The same 3 %/$5 transfer fee applies. Discover it® Cash Back gives 15 months at 0 % and rotates 5 % categories such as grocery stores, gas stations, or streaming services each quarter. New cardholders receive an uncapped dollar-for-dollar match of all cash back earned during the first 12 months, essentially doubling the yield to 10 % in the bonus categories and 2 % elsewhere. The transfer must be initiated within the first three months to secure the 0 % rate and 3 % fee. Bank of America® Customized Cash Rewards dangles 15 billing cycles at 0 % on transfers executed within 60 days. Users pick one 3 % category—gas, online shopping, dining, travel, drug stores, or home-improvement stores—and automatically earn 2 % at wholesale clubs and grocery chains on the first $2,500 of combined quarterly spending. A $200 online bonus is available after $1,000 of purchases in the first 90 days, effectively offsetting the 3 % balance-transfer fee on up to $6,666 of debt. No-Annual-Fee Options for Conservative Spenders American Express Blue Cash Everyday® carries no annual fee and grants 15 months of 0 % APR on both purchases and transfers with a 3 %/$5 fee. Ongoing rewards include 3 % at U.S. supermarkets, U.S. gas stations, and U.S. online retail purchases (each capped at $6,000 per calendar year, then 1 %). Because Amex prohibits transfers from existing Amex accounts, the card is best suited for people who carry higher-rate Visa or Mastercard debt. Citi Simplicity® and BankAmericard® likewise waive yearly charges, so consumers who pay off balances in full during the promo period never owe the issuer a dime beyond the one-time transfer fee. How Issuers Treat Transfer Windows and Fees in 2026 Promotional windows now start only when the account is opened, not when the first transfer posts. That means a 21-month offer ticks down even if the borrower waits four months to move the balance. Every card on the 2026 roster also imposes a minimum transfer fee—typically $5—even on small balances, so moving $300 still costs $9 on a 3 % card instead of the mathematically correct $9. After the deadline, fees usually jump one percentage point: BankAmericard® shifts from 3 % to 4 % after day 60; Citi products rise from 3 % to 5 % after month 4. Penalty pricing has largely disappeared among major issuers, yet a single 30-day-late payment on any of these cards can forfeit the 0 % rate and trigger a variable APR that immediately approaches 30 %. Real-World Savings: Running the Numbers on a $9,500 Balance Federal Reserve data peg the average household card debt at $9,480. Assume that balance compounds at 22 % with the borrower affording $400 a month. Without a transfer, the debt survives 31 months and accumulates $2,990 in interest. Moving the entire tab to Citi Simplicity® costs a $285 fee (3 %) and, if the $400 payment continues, the balance disappears in 24 months with no interest at all. Net savings equal $2,705, even after the upfront charge. A household that can manage only $275 a month would still wipe out $6,600 of principal during the 21-month Citi runway. The remaining $2,900 begins accruing interest at 18.99 %, yet the total finance charge is under $210—roughly $2,780 less than the status quo. Credit-Score Thresholds and Approval Realities Issuers typically reserve the longest 0 % offers for consumers with FICO scores of 720 or higher. Data from Experian show that 59 % of applicants in the 740–799 band were approved for the U.S. Bank Shield™ 24-month product in the final quarter of 2025, while only 27 % of those between 670–739 received the same terms; the latter group was often counter-offered a 12-month promo or an APR that started at 21 %. Utilization ratio plays an equally decisive role. A candidate with an 800 FICO but $35,000 in existing revolving balances across $40,000 of limits may still be declined because the new card would push combined utilization past 90 %. Conversely, a 695 FICO applicant who carries $4,000 on $20,000 of limits can be approved if income documentation supports the planned payoff schedule. Six Moves to Safeguard the 0 % Window Automate at least the minimum payment within five days of the statement date; on most cards any late payment voids the promotional APR the same day. Disable autopay for the old card only after the transfer posts and the issuer confirms a zero balance; otherwise residual interest or late fees can reappear. Divide the transferred amount by the number of promo months minus one, then round up to the nearest $25; the cushion ensures the balance expires one cycle early and absorbs any surprise fee. Refrain from new retail spending on the transfer card unless you can pay it in full each month; purchase APRs are not always set at 0 % even when transfers are. Keep the old account open if there is no annual fee; closing it slashes available credit and spikes utilization, which can drop a FICO score 25–40 points overnight. Schedule a calendar alert 60 days before the promo ends; if a balance remains, consider a second transfer or a low-rate personal loan before the revert APR applies. Alternatives When a Transfer Offer Falls Through Credit-union-sponsored personal loans averaged 10.9 % APR in February 2026, according to the National Credit Union Administration. A five-year, $10,000 loan at that rate costs about $217 a month and accrues $3,020 in interest—still cheaper than leaving the debt on a 22 % card making only minimum payments. Borrowers with sub-700 scores can turn to secured loans or 401(k) loans, though both entail collateral or retirement-plan risk. Nonprofit credit-counseling agencies can enroll consumers in debt-management plans that slash existing APRs to 6 %–8 % across all cards, but participants must close the accounts and forgo new credit for up to five years. Useful Resources Consumer Financial Protection Bureau: Download the “Paying Off Credit Card Debt” worksheet to build a month-by-month calendar tied to any intro period. AnnualCreditReport.com: Claim free weekly Equifax, Experian, and TransUnion reports required for pre-qualification screening. Experian Boost: Add utility and streaming payments to thicken your credit file before applying for premium 0 % offers. Bankrate Credit Card Payoff Calculator: Enter balance, APR, and monthly payment to compare transfer savings side-by-side with the status quo. National Foundation for Credit Counseling: Speak with an accredited counselor if balances exceed 40 % of annual income or approval odds appear slim.

Debt management and credit building

Debt management and credit buildingPay Off Credit Card Debt Fast With a Financial Windfall: Interest Savings Guide

A $1,000 tax refund, a $5,000 year-end bonus, or even a six-figure inheritance can feel like money dropped from the sky, yet the real test starts the moment it lands in your checking account. With U.S. credit-card balances still climbing—Federal Reserve data released in February 2026 puts the national total at $1.21 trillion—millions of households are one unexpected deposit away from wiping out years of high-interest drag. Deciding whether to extinguish that drag or to divert the cash elsewhere is less intuitive than it seems.Credit-Card Debt Destroys Wealth Faster Than Other LoansRevolving plastic carries the steepest borrowing cost most consumers will ever face outside payday storefronts. The average assessed interest rate on credit-card accounts that assess interest closed 2024 at 23.5 percent, more than triple the 7.2 percent average on 48-month new-car loans and nearly double the 12.7 percent fixed rate for federal undergraduate Stafford loans disbursed last school year. Unlike installment debt, cards compound daily, so every statement cycle that you roll a balance the lender recalculates interest on yesterday’s interest. A $7,500 balance left untouched at 23.5 percent balloons by roughly $1,770 in finance charges over twelve months—money that produces no new goods, services, or tax deductions.The asymmetry is what makes windfalls so powerful. Because the same dollar cannot simultaneously earn 5 percent in a high-yield savings account and avoid 23.5 percent in credit-card interest, the “return” you achieve by retiring the higher-rate obligation is guaranteed, tax-free, and immediate. Financial planners call this an arbitrage payoff: you capture the spread without market risk.One Lump Sum Can Rewrite Your Payoff CalendarConsider a borrower who owes $7,500 across three cards, all at 23.5 percent, and who can budget $200 a month toward reduction. Making the minimum on each and targeting the highest-rate card first—the avalanche method—would still require sixty-nine months to reach zero, during which the issuer banks about $6,050 in interest. Inject a $3,000 windfall in month one and continue the same $200 monthly outlay; the debt disappears in thirty-one months and total interest falls to roughly $1,550. That single decision frees thirty-eight months of cash flow and saves $4,500—money that can later fund retirement, college, or a down payment.The math tightens further if the cardholder can pair the windfall with a balance-transfer offer. Rolling the remaining $4,500 onto a fifteen-month 0 percent card and paying $300 a month eliminates the balance in fifteen months with zero interest. Total interest saved: $6,050. Total time in debt: cut by more than half.When Experts Say Keep the Debt—And the CashPayoff calculators make extinguishing balances look like a slam-dunk, yet planners routinely recommend that clients split windfalls. The reason is opportunity cost. A household with no emergency cushion risks falling back into expensive debt the next time the transmission fails or the dog swallows a sock. “We see it constantly,” says Phoenix-based CFP Miriam Ragan. “Client wipes out $10,000 on Visa, then six months later puts $4,000 on the same card at 24 percent because the roof leaked.” Ragan’s rule of thumb: reserve one month of core expenses in a high-yield savings account before attacking revolving balances. After that, each additional $1,000 of windfall gets a 75-25 split—75 percent to the card, 25 percent to cash—until the emergency fund covers three months. Only then does 100 percent flow to debt.Employer-matched retirement contributions create another exception. A worker who receives a $4,000 bonus forgoes a 100 percent immediate return if he neglects his 401(k) match to delete a 23 percent card. In that scenario, advisers tell him to contribute enough to capture the full match, then send the residual to the card company.Four Competing Goals That Also Deserve a SliceEmergency liquidity. Forty percent of adults surveyed by U.S. News & World Report in January 2026 said they could not handle a $1,000 surprise bill without borrowing. If your household falls in that cohort, seeding an online savings account yielding 4.5 percent beats the psychological relief of a zero balance that might not last.Student-loan acceleration. Federal undergraduate loans disbursed since 2023 carry fixed rates between 5.5 and 8.05 percent; older graduate PLUS loans can exceed 8.5 percent. Although those rates sit below today’s credit-card norm, the differential narrows when borrowers qualify for student-loan interest deduction (up to $2,500 yearly). Run an amortization schedule: if the effective after-tax rate on the student loan is within three percentage points of the card, wipe out the plastic first, then snowflake the freed payment toward the education debt.Retirement catch-up. The IRS kept 401(k) contribution limits at $23,500 for 2026 but indexed IRA caps to $7,000. Someone age fifty or older can add another $1,000. A $5,000 windfall dropped into a Roth IRA at age thirty-five growing at 7 percent real becomes $38,000 by age sixty-five—tax-free. That long-term leverage argues for at least partial funding before extra mortgage or low-rate student-loan prepayments.College inflation hedge. Fidelity’s 2025 College Savings Indicator found that 77 percent of parents are saving for tuition, yet projected future costs still outstrip their trajectory by 37 percent on average. Funding a 529 plan offers state-tax deductions in thirty-four states and tax-free growth for qualified withdrawals, but the benefit is time-sensitive; a ten-year horizon warrants higher priority than a two-year window.Two Lower-Cost Escape Hatches If No Windfall ArrivesConsumers who cannot count on an inheritance or bonus can still manufacture relief:Personal-loan consolidation. Origination volumes at online lenders rose 12 percent in 2025 as borrowers with 720-plus FICO scores locked three-year fixed rates near 11.5 percent—roughly half the current card average. Use the proceeds to zero out balances, then automate the installment payment. The fixed term imposes discipline that revolving lines lack.Zero-percent balance-transfer cards. Offers lengthened during 2025; issuers such as Wells Fargo and Bank of America dangle 0 percent APR for eighteen billing cycles with a 3 percent transfer fee. Someone who moves $6,000 and pays $350 a month retires the balance during the promo window, effectively borrowing eighteen months for a one-time 3 percent upfront charge—an annualized cost below 2 percent.Craft a Windfall Allocation Plan Before the Money HitsBehavioral-finance studies show that people spend found money faster than earned money when no plan exists. Draft your allocation percentages in advance: perhaps 50 percent to credit cards, 20 percent to emergency savings, 15 percent to retirement, 10 percent to college, and 5 percent to discretionary splurge. Email the recipe to yourself or a trusted friend; when the refund or bonus arrives, execute within forty-eight hours before lifestyle creep whittles the surplus. Automation matters: schedule the card payoff online the same day the ACH clears so that the statement balance updates before temptation strikes.In Toledo, Ohio, for instance, 29-year-old warehouse supervisor Carlos Vega received a $3,200 tax refund in March 2025. He had $6,800 spread across four cards at 24 percent APR and only $400 in savings. Vega pre-wrote a plan: 60 percent to the highest-rate card, 25 percent to emergency cash, 10 percent to a Roth IRA, and 5 percent to “fun.” He moved the money the same day the refund hit; by June his utilization ratio dropped from 88 percent to 42 percent, and his FICO score jumped 46 points. The quick victory, he says, “made the plan feel real.”Finally, log the victory. Download your free credit report three months after the big payment; watch utilization fall and scores climb. The average consumer who eliminates 60 percent of revolving balances sees a forty-point FICO gain within two cycles—cheaper insurance premiums, better refinance offers, and the satisfaction of knowing the windfall kept working long after the balance hit zero.Useful ResourcesAnnualCreditReport.com – Official gateway to pull your Equifax, Experian, and TransUnion reports weekly at no charge; monitor balance updates after payoff. FDIC Credit-Card Repayment Calculator – Interactive tool that shows how lump-sum payments alter payoff horizons and interest cost under various APRs. Vanguard Emergency-Fund Planner – Worksheet that matches monthly core expenses to recommended savings tiers and suggests high-yield money-market options. Federal Student Aid Loan Simulator – Government calculator that estimates effective after-tax rates on education debt, helping prioritize versus credit-card payoff. Savingforcollege.com 529 Map – State-by-state listing of tax deductions, credits, and minimum contributions for college-savings plans.Source: Original reporting and public data from the Federal Reserve, U.S. Department of Education, and interviewed certified financial planners.

Debt management and credit building

Debt management and credit buildingCredit Card Consolidation: How to Combine Balances and Cut Interest Costs