Retirement savings benchmarks show that a 30-year-old earning the national average should already hold roughly $85,000 in tax-advantaged accounts, while a 60-year-old should have amassed about eight times final salary—currently translating to just under $780,000—to stay on track for a 30-year post-work life, according to Fidelity data updated for 2026 wage levels.

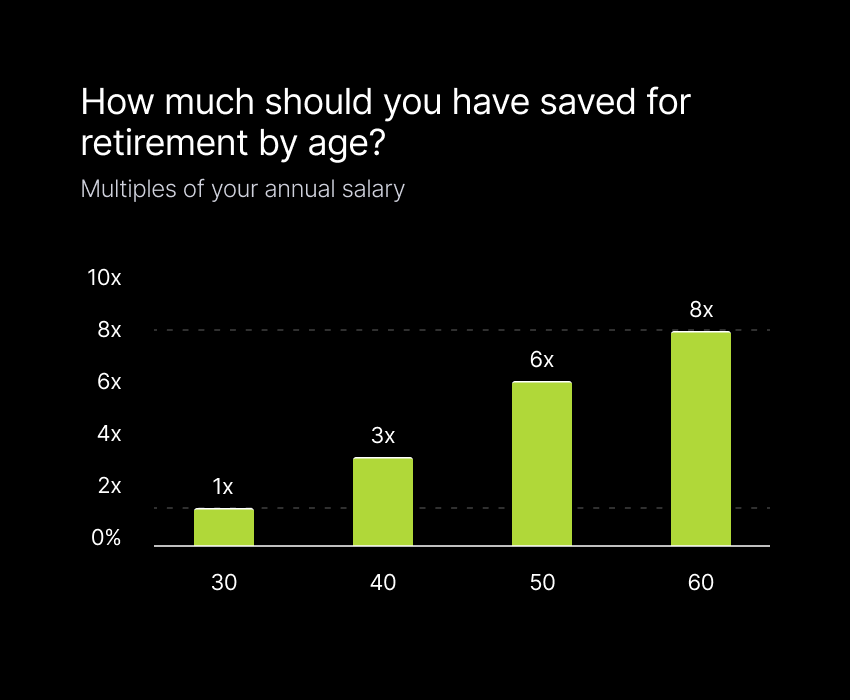

Fidelity Age-Based Savings Roadmap

Fidelity’s model assumes career-long contributions of at least 15 percent of pretax pay, including employer matches, and portfolio growth near the historical 7 percent annualized equity return. Milestones therefore rise steeply: one-times salary at 30, three-times at 40, six-times at 50 and eight-times at 60. The math treats each multiple as a checkpoint, not a finish line, because Social Security will replace only about 35 percent of median earnings. Missing a checkpoint compounds the shortfall; a worker who reaches 40 with only double her $109,000 salary instead of triple must save roughly 22 percent of pay for the next decade to claw back the gap, Fidelity calculates.

In Dayton, Ohio, for instance, a public-school teacher who met the 30-year mark dead-on found herself sidetracked by two maternity leaves and a mortgage refinance; she is now 42 and contributing 18 percent of pay plus a 5 percent match to regain lost ground.

Why the Numbers Feel Impossible in 2026

Median weekly earnings have climbed 18 percent since 2020, yet the average 401(k) balance for savers in their thirties has grown just 11 percent after market swings, Vanguard’s latest How America Saves report shows. Student-loan payments resumed in late 2023, siphoning $260 a month from the typical household budget, while median rent crossed $1,400 nationally. “People look at the age targets and freeze,” says Cincinnati financial planner Tiya Lim, noting that the psychological hurdle often deters contributions altogether. Behavioral economists add that loss-aversion is amplified when the goalpost appears to move faster than income.

Critics argue the benchmarks overlook regional cost gaps; a $78,000 salary stretches further in Memphis than in San Diego, yet the multiple stays the same.

Emergency Buffer: Three to Six Months of Core Costs

Separate from retirement, advisers urge workers to stockpile three-to-six months of non-discretionary spending—housing, utilities, insurance, groceries, transport and minimum debt service—in high-yield savings or money-market funds now paying 4.2 percent on average. Using 2023 Consumer Expenditure Survey data updated for 2026 price levels, that equals roughly $18,000-$36,000 for 30-year-olds, $23,000-$45,000 for 40-year-olds, $24,000-$49,000 for 50-year-olds and $21,000-$42,000 for 60-year-olds. Frontier Investment Management senior planner Sergio Garcia recommends targeting the lower figure for dual-income households and the higher sum for single earners or those in cyclical industries.

Meanwhile, unexpected layoffs in the tech sector this spring have underscored the value of keeping the cushion in an account that can be tapped within one business day.

Catch-Up Tactics If You’re Behind

Workers over 50 can funnel an extra $7,500 into 401(k)s and $1,000 into IRAs on top of standard 2026 limits. Automating a one-percent-of-pay raise each year—often called a “save more tomorrow” escalation—has been shown to triple 10-year balances in University of Chicago field studies. Side-gig income can be deposited directly into a solo 401(k), sheltering up to 25 percent of net self-employment earnings. Younger savers can front-load Roth contributions while tax brackets are lower, locking in decades of tax-free growth. Finally, refinancing high-interest credit-card balances to fixed personal loans near 8 percent frees median $340 monthly that can be redirected to retirement without crimping cash flow.

Separately, some employers now allow after-tax 401(k) contributions that can be instantly converted to Roth inside the plan, a maneuver that unexpectedly boosted one Denver engineer’s balance by $19,000 last year alone.

Useful Resources

- Fidelity Retirement Score – Free 10-question tool that projects whether your savings will cover planned expenses.

- Consumer Financial Protection Bureau Emergency Savings Guide – Printable worksheet to calculate exact three- and six-month targets by ZIP code.

- Vanguard Investor Questionnaire – Assesses risk tolerance and suggests target-date fund allocation aligned with your horizon.

- IRS Retirement Plans FAQs – Official 2026 contribution limits, catch-up rules and tax-deduction phase-outs.

Sources: Fidelity Investments 2026 Retirement Savings Guidelines; Vanguard How America Saves 2026; U.S. Bureau of Labor Statistics Consumer Expenditure Survey; Federal Reserve Economic Data.

Comments