Only 41 percent of U.S. adults can pay a surprise $1,000 bill from savings, Bankrate’s 2025 Emergency Savings Report shows. That stark figure underscores why setting a monthly savings target—however modest—remains the first concrete move toward breaking the paycheck-to-paycheck cycle.

Why the 15–20% Rule Still Dominates Advice

Certified financial planners have long preached the gospel of siphoning off 15–20 percent of gross income before living expenses even register. The range is not arbitrary: it captures the average amount needed to fund a 30-year retirement at 80 percent of pre-retirement income while simultaneously building a liquidity cushion. Laura Davis, CFP and founder of Financial Labs Inc., cautions that the ratio “works best for households with stable wages and employer retirement matches already baked in.” Translation—if your 401(k) receives a 4 percent company match, only 11 percent more is required from your own pocket to land inside the band. The figure also folds in health-savings-account deposits, 529 college contributions, and extra mortgage principal, not just idle cash in the bank.

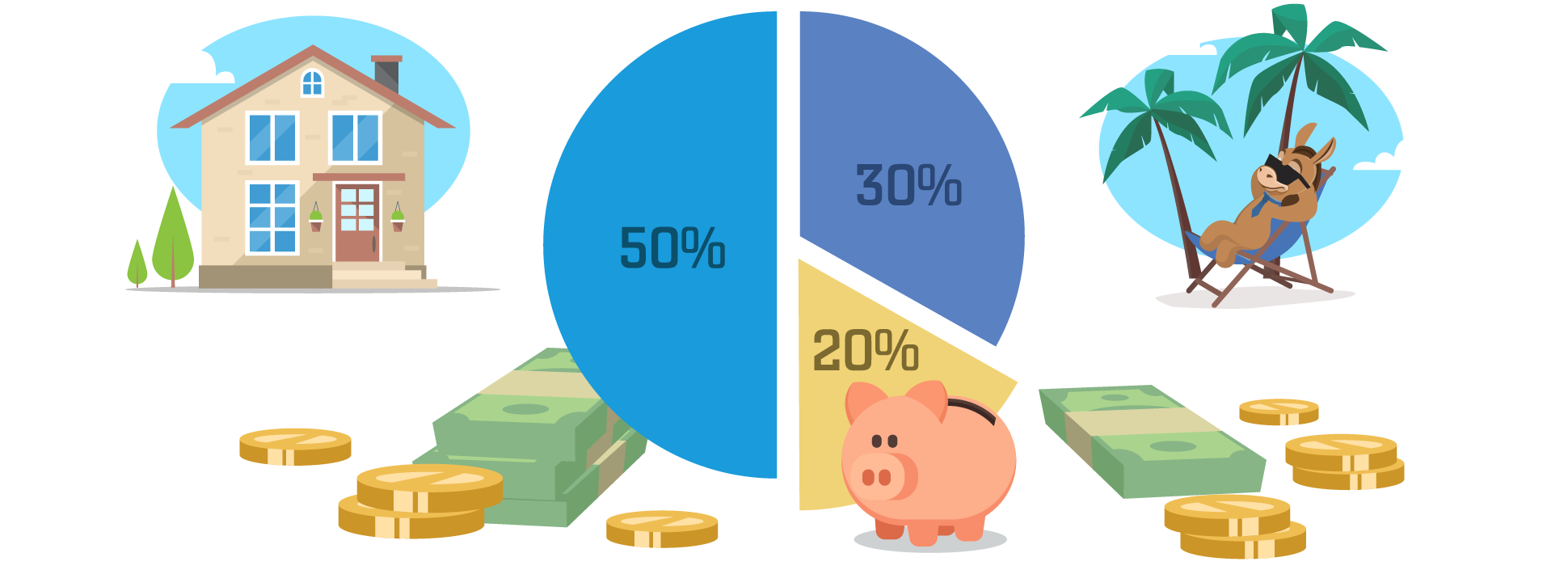

How the 50/30/20 Budget Handles Savings

For savers who think in percentages of take-home pay, the 50/30/20 rule offers a lighter mental lift. Half of net income covers needs—rent, utilities, insurance minimums—while 30 percent funds discretionary wants. The remaining 20 percent is earmarked for “financial priorities,” a bucket that blends saving and debt payoff. A household clearing $4,500 after taxes would therefore route $900 a month toward Roth IRA deposits, emergency-fund transfers, and additional student-loan principal. Behavioral economists like the rule because it forces trade-offs inside each silo; overspending on restaurants cannot leak into rent money, and the 20 percent floor keeps savings on autopilot even when income rises.

Tailoring the Percentage to Your Income Tier

Low-income families often confront a mismatch between fixed costs and earnings; rent alone can exceed 40 percent of gross pay. Advisors recommend an initial savings rate of 5–10 percent directed solely into a starter emergency fund—usually one month of core expenses—held in a high-yield online account currently paying 4–5 percent APY. Middle-income earners—roughly $55,000–$120,000 for a dual-income household—can ratchet the rate toward 15 percent once high-interest credit cards are tamed. High earners face the opposite risk: lifestyle creep. Pushing the savings rate above 20 percent captures additional tax-deferred space—think 403(b) and mega-backdoor Roth strategies—while insulating portfolios from sequence-of-returns risk decades before retirement.

Where to Park the Cash for Maximum Growth

Account selection matters as much as the dollar amount. Emergency reserves belong in FDIC-insured high-yield savings or money-market accounts where daily liquidity is guaranteed and interest compounds daily. Goal-specific money needed within three years—say, a car replacement—can tolerate a short-term Treasury ETF sporting slightly higher volatility but negligible credit risk. Retirement dollars should ride equity index funds inside tax-favored wrappers; a 25-year-old earning 7 percent real returns turns $500 monthly into roughly $790,000 by age 60, compared with $290,000 in a 0.5 percent savings account. Health savings accounts, often overlooked, offer triple tax advantage and can double as stealth retirement vehicles after the emergency benchmark is met.

Rebalancing Your Rate as Life Evolves

Savings targets are not static. Marriage, home purchases, or a shift to freelance income should trigger a fresh calculation. A simple annual audit—add up all household cash-flow surpluses, divide by gross income, compare with the prior year—keeps the percentage honest. Automate escalation: schedule 1 percent increases every six months until the ceiling feels tight, then pause. Finally, redirect windfalls—bonuses, tax refunds, restricted-stock vests—before they reach checking accounts; behavioral research shows once money is labeled “spendable,” the psychological hurdle to move it skyrockets.

Emergency-Fund Benchmarks by Life Stage

Critics argue the classic “three-to-six months of expenses” mantra glosses over real-world volatility. In practice, single renters with robust health coverage can land on the lower end, while dual-income parents with a mortgage and childcare bills often stockpile nine months. Unexpectedly, the rise of gig work nudges the target higher still; freelancers in Austin, for instance, report saving 12 months of overhead after 2023’s tech-contract freeze.

Automation Tools to Keep You Honest

Fintech apps such as Qapital and Ally Bank’s Surprise Savings algorithm sweep micro-amounts into sub-accounts every few days, trimming the temptation to spend. Meanwhile, employer payroll portals increasingly allow split deposits across four or more institutions, letting workers siphon retirement, emergency, and vacation funds before the net paycheck even lands.

Tax-Sheltered Options Beyond the 401(k)

Once the emergency fund is flush, extra cash can flow into a Roth IRA (2026 limit: $7,000 under 50) or, for high-deductible health plans, an HSA (contribution cap: $4,150 individual, $8,300 family). Both vehicles grow tax-free, and the HSA allows penalty-free withdrawals for any purpose after age 65, making it an unexpectedly flexible pot of money.

Useful Resources

- Bankrate 2025 Emergency Savings Report – Full survey data on American saving habits and breakdowns by age and region

- NerdWallet 50/30/20 Calculator – Interactive spreadsheet that auto-splits net income into the three buckets and graphs progress

- TreasuryDirect.gov – Purchase 4-, 8-, 13-, or 26-week Treasury bills online with no brokerage fees for short-term surpluses

- Vanguard Roth IRA Starter Kit – Step-by-step guide to opening, funding, and selecting low-cost index funds within IRS limits

Comments