At 40, Retirement Math Meets Reality: Gap Tops $120,000 as Fed Data Show Median Household Has Only $60,000 Saved

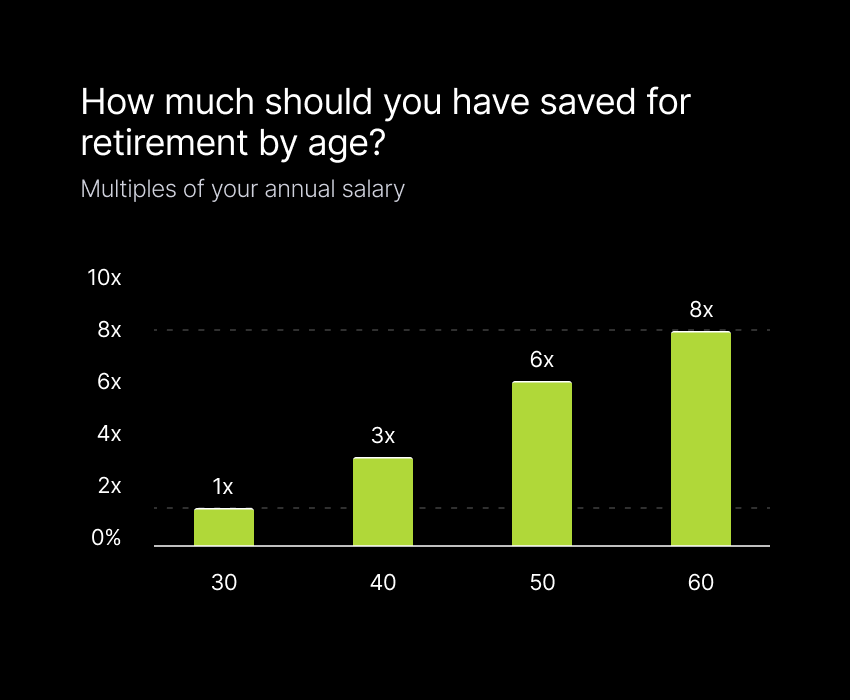

The 3× Salary Rule in 2026 Dollars

Fidelity’s guideline—three times annual salary tucked away by age 40—now equals about $126,000 for the median individual and $240,000 for the median household. The estimate assumes steady contributions from age 25, a 5 percent employer match, and market returns near their 100-year average. Miss one leg of that stool and the target moves. Lauryn Williams, a Dallas CFP and former Olympic sprinter, calls the rule “a compass, not a contract,” and tells clients to reset the number every 24 months. A promotion, layoff, or six-month caregiving break can swing the goal by tens of thousands before the next tax season. Inflation adds another twist: the 2022-2024 spike shaved 18 percent off the buying power of a $240,000 nest egg, Bureau of Labor Statistics data show.

What the Fed’s 2022 Survey Really Says About 40-Somethings

The Survey of Consumer Finances pegs mean net worth for households headed by someone aged 40-44 at $1.06 million, yet the median 401(k) balance is only $60,000. The gap traces to business equity and home values—assets you cannot tap for groceries without selling or borrowing. Empower’s 401(k) database, covering 2.8 million participants, shows a median balance of $232,000 for workers who stay with one employer for at least ten years, but that group is just 28 percent of the labor force. Once job-hoppers, freelancers, and caregivers are added, the flashy six-figure balance becomes the exception, not the norm.

Eight Moves to Close the Gap Before 50

Financial planners frame the decade between 40 and 50 as an eight-step sprint. Each tactic is ranked by the dollars it can realistically add by your fiftieth birthday, assuming you start today.

Step 1: Write the Day-in-the-Life Script

Peter Lazaroff, CFA and host of the Long-Term Investor podcast, asks clients to draft a one-page story: where they wake up at 65, what they spend in a week, and which income streams arrive. A couple that needs $7,000 a month after tax and expects $3,200 from Social Security must still pull $3,800 from portfolios—about $1.4 million using a 3.5 percent withdrawal rate. Once the figure is concrete, the monthly savings rate becomes negotiable instead of mythical.

Step 2: Push Income First, Budget Second

Atlanta Fed wage data show job-switchers in their 40s earn 7.3 percent raises on average versus 4.1 percent for stay-puts. A $12,000 bump directed into a 401(k) for eight years grows to roughly $140,000 at a 7 percent return, wiping out the typical shortfall without trimming lattes.

Step 3: Build a Seven-Month Cash Wall

Bankrate finds 38 percent of adults would borrow or sell something to cover a $1,000 surprise. A high-yield online account—still paying 4 percent or more as of March 2026—prevents raids on retirement funds that trigger taxes and a 10 percent penalty if you are under 59½.

Step 4: Hack the Match Calendar

One in five plans still credits the full match only if you contribute every pay period. Others “true-up” the next spring. Ask HR which camp you’re in; if it’s the latter, you can max the 401(k) by October and free up cash for holidays without forfeiting free money.

Step 5: Run the HSA Triple Play

High-deductible plan holders can stash $4,850 individual or $8,750 family in 2026. Money goes in pre-tax, grows tax-free, and comes out tax-free for medical bills—an expense Fidelity projects will eat 15 percent of the average retiree’s budget. After 65, leftover dollars behave like 401(k) funds: taxable but penalty-free.

Step 6: Delete 8 Percent Drag Before Chasing 8 Percent Returns

Private student loans still hover near 7-9 percent. Paying off an 8 percent note delivers a risk-free 8 percent return, a bar the S&P 500 has cleared in only 60 percent of rolling five-year periods since 1950. Tony Steuer, author of Get Ready!, advises wiping out anything above 6 percent before raising 401(k) contributions beyond the match.

Step 7: Just Say No to the College Guilt Trip

A 2025 Sallie Mae study shows 43 percent of parents yank money from retirement to pay tuition. Students can borrow for college; retirees cannot borrow for groceries. Brent Weiss, CFP and co-founder of Facet, frames securing your own retirement first as “an act of love, not selfishness,” because it prevents your kids from bankrolling you later.

Step 8: Buy Advice by the Hour

A 1 percent wrap fee on $300,000 costs $30,000 a decade—money that could stay invested. Flat-fee planners charge $2,500-$4,000 for a comprehensive plan, a model that turns cheaper once assets top $250,000. The break-even arrives faster than most investors expect, especially when portfolios hold low-cost index funds that need little tinkering.

Why the Average 40-Year-Old Portfolio Is 73 Percent U.S. Equity

Target-date funds for 2045 retirees allocate 73 percent to domestic stocks, 18 percent to foreign developed, 4 percent to emerging markets, and 5 percent to bonds, Morningstar reports. The blend has returned 8.9 percent annually since 1988 but also produced a 35 percent drawdown in 2008 and a 24 percent drop in 2020. Advisors now add “flex buckets”—cash-value life insurance or rental equity—that can be tapped during crashes so clients aren’t forced to sell shares at trough prices. Weiss recommends stress-testing your mix against a 30 percent plunge; if the hypothetical loss ruins your sleep, the allocation is wrong no matter what the textbook says.

Social Security, Taxes, and the 40-Something Window

Full retirement age is 67 for anyone born 1960 or later, yet benefits can start at 62. Each year you wait past 67 adds 8 percent in inflation-adjusted income for life—an implied real return unavailable in today’s bond market. For couples, the higher earner’s benefit survives the longest, making that delay the most valuable. But the decision collides with tax rules: once combined income tops $44,000, up to 85 percent of Social Security becomes taxable. Roth conversions in your 40s and 50s let you pre-pay tax at today’s rates, then draw tax-free income that won’t trigger benefit taxation later. Converting $50,000 a year for eight years costs roughly $12,000 in federal tax for someone in the 24 percent bracket yet can avert $300,000 in taxable required minimum distributions later, Schwab projections show.

Lifestyle Creep and the $12 Cocktail Problem

Inflation-adjusted median household income has climbed 14 percent since 2019, yet the personal-savings rate fell below 4 percent in late 2025, down from a 2020 peak of 17 percent. Subscription stacking, food-delivery surcharges, and “small luxury” inflation are the culprits. Two $12 craft cocktails a week plus a $65 streaming bundle totals $3,800 a year—money that, invested at 7 percent, grows to $55,000 in ten years. Track every swipe for 90 days and you will find 6-9 percent of after-tax income leaking into such invisible buckets, JPMorgan Asset Management finds. Redirecting half of that plug closes the retirement gap for 60 percent of households.

The Gender Gap at 40: Data Behind the Headlines

Women aged 40-44 hold 78 cents in retirement assets for every dollar held by men, Vanguard’s 2025 How America Saves reports. Career breaks explain 56 percent of the gap; wage disparities, 31 percent; lower equity allocations, 13 percent. Fixes are tactical: spousal IRAs during maternity leaves, auto-escalation plans that restart 1 percent higher after any pause, and employers such as IBM and Patagonia that credit 401(k) matches during six-month parental leaves. A “phantom year” policy can add $18,000-$25,000 to a 40-year-old woman’s balance overnight.

Remote-Work Windfalls and Geographic Arbitrage

Twenty-two percent of U.S. workers are fully remote as of 2026, up from 5 percent in 2019. Relocating from a $4,200-a-month San Jose apartment to a $1,800 Raleigh mortgage frees $28,800 after tax—enough to max out a 401(k), a Roth IRA, and still pay for a week at the beach. Cost-of-living calculators show a $150,000 Austin salary equals $246,000 in Manhattan; locking in a location-adjusted paycheck while pocketing the savings turbocharges retirement funding without lifestyle sacrifice. U-Haul’s 2025 migration report ranks Tennessee and North Carolina as top destinations for 35- to 44-year-olds, citing zero state income tax in Tennessee and cheaper housing.

Action Steps

- Run a free retirement calculator (AARP, Vanguard, or Empower) tonight; scribble the gap on a sticky note and park it on your mirror.

- Bump your 401(k) deferral by 1 percent this quarter—even if you’re still paying down 6 percent debt; the tax break dulls the sting.

- Email HR for a 30-minute call to nail down match timing rules and whether after-tax in-plan Roth conversions are allowed.

- Open a high-yield savings account labeled “Emergency Only” and feed it this year’s tax refund; autopilot $250 a month until you hit seven months of core expenses.

- Book a flat-fee CFP for a two-hour portfolio physical before your next birthday; bring last year’s tax return, a current pay stub, and a list of every investment account—including the 403(b) you forgot exists.

Useful Resources

- Empower Retirement Planner Calculator – Aggregates accounts and runs Monte Carlo projections in under five minutes.

- National Association of Personal Financial Advisors (NAPFA) – Locates flat-fee, fiduciary planners by ZIP code.

- Social Security Administration Quick Calculator – Projects monthly benefits at 62, 67, and 70 using your actual earnings record.

- Vanguard Target-Date Fund Glide Path White Paper – Lists exact stock-bond mix for every vintage and why.

- HSA Search – Compares fees and investment menus among 350-plus health-savings providers.

Sources: Federal Reserve Survey of Consumer Finances 2022, Vanguard How America Saves 2025, Morningstar 2025 target-date universe, Bureau of Labor Statistics CPI and employment reports, JPMorgan Asset Management 2024 behavior-finance study, Schwab Center for Financial Research projections, Atlanta Fed wage-growth tracker, Bankrate emergency-savings survey, Sallie Mae How America Pays for College 2025, U-Haul 2025 migration study.

Comments