Anyone with a giving budget can open a donor-advised fund—no private foundation required. The vehicle is now the fastest-growing philanthropic account in the United States because it bundles immediate tax relief with years-long payout flexibility, Fidelity Charitable reports.

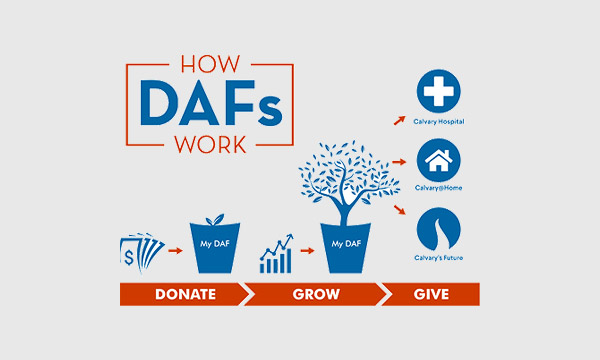

How a donor-advised fund actually works

You open the account at a sponsoring 501(c)(3)—a community foundation, university, or the charitable arm of a brokerage such as Schwab, Fidelity, or Vanguard.

Your opening gift can be cash, appreciated stock, cryptocurrency, even shares of a privately held company.

The sponsor immediately legalizes the transfer, making it irrevocable; you, however, retain the right to recommend future grants to any IRS-qualified public charity.

Because the assets now belong to the sponsor, you receive the full charitable deduction in the year you fund the account, provided you itemize deductions on Schedule A.

Tax math you must clear first

The deduction only helps if your total itemized deductions surpass the standard deduction set each year by the IRS.

For the 2023 filing season that meant topping $13,850 for single filers or $27,700 for joint filers; in 2024 the bar rises to $14,600 and $29,200 respectively.

Taxpayers who bundle several years of giving into one “bunching” year frequently clear the threshold, then glide back to the standard deduction in off-years.

Offsetting up to 30 percent of adjusted gross income with long-term appreciated securities, or 60 percent with cash, can further trim lifetime tax drag.

Any unused deduction can be carried forward for five additional tax years, giving households runway to stagger the benefit.

Growth engine inside the account

Assets you do not grant out remain invested in pools resembling mutual funds or ETFs—often with expense ratios below 0.20 percent at large commercial sponsors.

Historical returns near 7 percent, net of fees, imply an untouched $25,000 block could double roughly every decade, magnifying future charitable impact without fresh deposits.

Sponsors typically offer risk-based models; aggressive choices suit donors who expect a long runway before distribution, while money-market sleeves work for imminent grant-makers.

All appreciation escapes capital-gains tax, so donating low-basis stock rather than selling it first eliminates the 15, 20, or 23.8 percent levy you would otherwise owe.

Control levers and legal limits

Although colloquially called “donor-controlled,” the law requires the sponsoring board to own final grant approval; variance power is rarely invoked except when a recommendation benefits a private individual or violates public-policy rules.

You may name successor advisers—spouse, child, grandchild—allowing multi-generational family philanthropy without the 5 percent annual payout imposed on private foundations.

Grants cannot reimburse you for gala tickets, pledge payments, or political campaigns, and you may not receive goods or services in return.

Most sponsors enforce a $50–$500 minimum grant size and allow international giving through intermediary charities, expanding the usable universe to thousands of nonprofits.

Cost profile vs. charitable trust

Opening minimums have fallen to zero at some digital-first platforms; household-name sponsors still hover between $5,000 and $25,000.

Annual administrative fees—often 0.60 percent on the first $500,000—drop on a sliding scale and are separate from the underlying investment expense.

By contrast, a charitable remainder trust demands attorney drafting, ongoing tax filings, and annual valuations, easily topping $5,000 in setup cost and hours of trustee labor.

Flexibility is another differentiator: donor-advised funds allow you to raise or lower annual giving to match cash-flow needs, whereas remainder trusts pay a fixed annuity and cannot accept additional contributions.

Action Steps

- Verify you will itemize deductions this year; if not, consider bunching two or three years of gifts into one deposit.

- Identify appreciated holdings in your taxable portfolio; transfer them in-kind to avoid capital-gains recognition.

- Compare sponsor investment menus and fee schedules; request a sample grant-approval timeline before opening.

- Draft a giving mission statement with family members, then schedule quarterly grant-review dates to keep the account active—most sponsors require at least one grant every five years.

Source: Fidelity Charitable 2024 donor-advised fund report

Comments