Budget Management and Cash Flow Budget Management and Cash Flow

Budget Management and Cash Flow

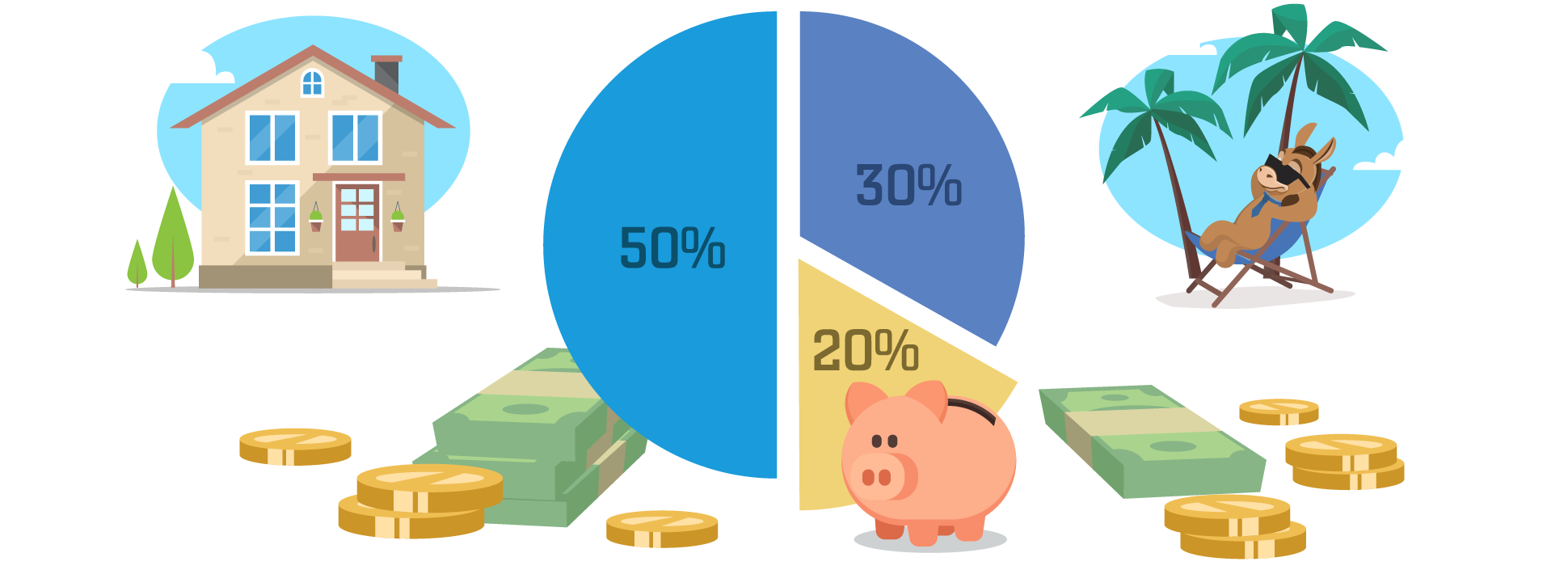

Budget Management and Cash Flow$100k Salary Budget Breakdown: How to Allocate Take-Home Pay

Net Pay Reality Check: A $100k Salary Shrinks to Roughly $75k After Taxes and Benefits, Forcing Tight Budget Choices A headline six-figure salary can feel like a lock on financial comfort—until the first direct deposit lands. After federal withholding, state income tax, FICA, Medicare surcharges, health-insurance premiums, and a 401(k) contribution, the $8,333 monthly gross on a $100,000 salary typically collapses to about $6,250 in take-home pay. In dollar terms, the popular “I make 100” boast is closer to “I live on 75,” and that 25 percent gap widens in high-tax jurisdictions. Critics argue the shrinkage is the clearest proof that “six figures” is no longer the safety blanket it once was. How $100k Turns Into $75k: Tax and Payroll Deductions The erosion starts with federal income tax. A single filer claiming the standard deduction owes roughly $13,500 for 2025, placing the marginal dollar of earnings in the 22 percent bracket. Add $7,650 in combined Social Security and Medicare (including the 0.9 percent Additional Medicare Tax that kicks in above $200,000 for joint filers), plus an average state income tax of 4 percent, and the visible subtractions already top 25 percent of gross. Yet the quiet killers are benefits. A mid-tier family PPO plan can cost $450 per paycheck; a 6 percent of salary 401(k) deferral lops another $500 off monthly cash flow; and ancillary products such as group life, disability, commuter benefits, and legal insurance nibble away another $120. The final stub in a place like Portland, Oregon, can show $5,850 net; in Miami-Dade, with no state income tax, the figure rebounds to $6,450. Either way, the advertised “$100k” is now a memory. Jamie Hobkirk, CFP, CFA, at Reynders, McVeigh Capital Management, tells clients to treat the missing slice as money already at work: “Every diverted dollar either cuts taxable income or buys an asset. The trick is to automate the diversion before your checking account tempts you.” Unexpectedly, she recommends new hires elect a higher-than-match 401(k) rate on day one; lifestyle then forms around the lower net, eliminating the agony of future budget cuts. Housing Reality: Keep Core Costs Below 30 Percent of Net Housing is the loudest line item in any budget, and lenders still quote the 28/36 rule—no more than 28 percent of gross income for the mortgage, 36 percent for all debt—even though underwriting software now approves borrowers up to 50 percent if credit scores exceed 760. On a $75,000 net, however, 30 percent equals $1,875 a month for rent or the full ownership bundle of mortgage, taxes, insurance, HOA, and minor maintenance. In Atlanta, that threshold finances a $285,000 home with 10 percent down and a 6.25 percent rate; in Seattle, the same payment covers a 480-square-foot studio in a 1960s walk-up. The geographic mismatch forces trade-offs. Hobkirk recently worked with a tech analyst who kept a San Francisco salary but relocated to Richmond, Virginia, slashing rent from $3,400 to $1,650 and banking the $20,000 yearly difference into a down-payment fund. Property-tax reassessment risk is under-reported. In Nashville, a 2024 city-wide reappraisal lifted the tax on a $400,000 bungalow from $3,200 to $4,100—an extra $75 a month—enough to nudge an otherwise prudent budget past the 30 percent red line. Buyers should stress-test a 20 percent tax hike before signing, not after. The 50-30-20 Rule Applied to a $75k Net Elizabeth Warren’s 50-30-20 framework—half for needs, 30 percent for wants, 20 percent for savings and accelerated debt payoff—translates to $3,125 for needs, $1,875 for wants, and $1,250 for wealth-building on a $6,250 monthly net. Childcare, car payments, and student loans, however, can hijack the formula. Minneapolis parents, for instance, pay a median $1,450 a month for toddler care, nearly half the “needs” allotment for one child. Rebalancing starts with variable essentials. USDA pilot data from 2025 show households using the Mealime app cut grocery costs 23 percent by trimming waste. Transportation offers another lever: swapping a 2021 Ford F-150 (18 mpg) for a 2023 Toyota Prius (57 mpg) saves $192 monthly at $3.30 per gallon and 1,200 miles driven. Those two tweaks alone free $310—enough to restore the 50-30-20 ratio without surrendering weekend sushi night. Emergency Fund: Nine Months of Core Costs Is the New Target Pre-pandemic planners preached three-to-six months of cash reserves; post-pandemic job volatility has stretched the target to nine months for single earners. Core spending of $4,500 a month therefore demands a $40,500 buffer—an intimidating mountain, yet reachable through micro-deposits. Automate a weekly $75 transfer to an online savings account yielding 4.5 percent APY; compounded monthly, the balance crosses $10,000 in 2.4 years without a single belt-tightening episode. Meanwhile, liquidity must coexist with high-interest debt eradication. When credit-card utilization tops 30 percent, redirect discretionary savings to an avalanche payoff; the 21 percent APR on rewards cards dwarfs the 4.5 percent earned in savings. Once balances fall below 10 percent, resume the automatic transfer schedule. This toggle keeps cash reserves intact while attacking the highest after-tax “return” available—eliminating expensive debt. Budget Frameworks: Zero-Based, Envelope, and Reverse Strategies Zero-based budgeting grants every incoming dollar a mission before the month begins, driving mindfulness at the cost of granular tracking. Apps such as YNAB import bank feeds and color-code underfunded categories in real time; users report a 17 percent spending reduction in the first quarter, per a 2025 survey of 4,800 paying subscribers. Cash loyalists still swear by the envelope system, now digitized. Goodbudget creates virtual envelopes synced across spouses’ phones; when the “Eating Out” envelope hits zero, the app declines the debit card, eliminating overdraft surprises. Reverse budgeting flips the sequence: fund goals first—retirement, vacation, down-payment—then live on the remainder. A $100,000 earner maxing a 401(k) at $23,000 and a Roth IRA at $7,000 must fit lifestyle into $45,000 net, forcing creative housing solutions such as co-buying with friends or accepting a 20-minute longer commute. Calendar Triggers and Life Events: When to Re-run the Numbers Budgets ossify without scheduled reviews. Link a quarterly calendar reminder to property-tax notices, insurance renewals, and open-enrollment windows. A 2 percent raise ($2,000 gross) should automatically escalate 401(k) deferrals by 1 percent and divert another 0.5 percent to a 529 college plan—strategies known as “raise parking.” Life events scramble assumptions: a July 2025 childbirth triggers $1,600 in new monthly expenses (diapers, formula, added health premium), but also a $2,000 child tax credit and $5,000 dependent-care FSA, net positive by $3,400 annually if cash-flowed correctly. Review subscription creep annually; the average consumer underestimates recurring charges by $79 a month, according to 2024 C+R Research. Canceling three dormant apps and renegotiating a $150 Comcast bill to $95 via the retention desk liberates $134—enough to fund a 529 plan at $100 and still pocket splurge money. Psychological Guardrails: Spending Speedbumps and Social Contracts Behavioral economists recommend “speedbumps” to slow impulse buys. Delete stored credit-card numbers from Amazon; the 30-second re-entry window cuts one-click purchases by 14 percent, per University of Chicago 2025 findings. Social contracts add accountability: share an annual savings target with two friends; group-chat progress each quarter. The American Savings Challenge reports participants save 28 percent more when progress is public. Visual cues matter. A wall chart coloring in each $1,000 of emergency-fund progress converts an abstract goal into a game, leveraging the endowed-progress effect—people accelerate effort when the finish line appears closer. Mini-Case Snapshot: One Couple, Two Cities, Different Outcomes In Denver, a newly married pair earns a combined $100,000—one spouse at a university, the other freelancing. By choosing a $1,600 two-bedroom in Aurora instead of a $2,400 loft downtown, they bank $9,600 a year. They divert the surplus to a high-yield savings account and max out two Roth IRAs. Meanwhile, in San Diego, a single software marketer making the same $100,000 pays $2,650 for a Mission Valley one-bedroom, leases a Tesla Model 3 for $499, and chips away at $38,000 in graduate debt. Despite identical gross pay, the Denver couple’s lower fixed costs create a $1,200 monthly wealth-building gap—proof that geography and fixed obligations, not salary alone, steer long-term security. Useful Resources (Plain Text) NerdWallet Budget Calculator – Interactive worksheet that converts gross pay to net and auto-applies 50-30-20 percentages.IRS Paycheck Checkup Tool – Estimates correct withholding to prevent year-end tax shocks.Consumer Financial Protection Bureau Housing Affordability Spreadsheet – Compares rent-vs-buy metrics city-by-city with property-tax history.YNAB Free 34-Day Trial – Zero-based app that imports bank feeds and color-categories underfunded envelopes.Vanguard Retirement Nest Egg Calculator – Projects 401(k) growth at various contribution rates, factoring employer match. Sources: Reynders, McVeigh Capital Management; USDA; C+R Research; American Savings Challenge; University of Chicago Booth School of Business.

Budget Management and Cash Flow

Budget Management and Cash FlowEnvelope Budgeting Explained: How the Cash Envelope Method Controls Spending

Without a written budget, even small daily purchases can snowball into credit-card balances, overdraft fees, and missed savings targets. The envelope budgeting method—whether executed with paper sleeves or inside an app—gives every dollar a single, visible assignment before the month begins, sharply reducing the risk of overspending.How Envelope Budgeting Assigns Every Dollar a JobAt its core, envelope budgeting is a pre-spending plan: net pay arrives, fixed costs such as rent and utilities leave the account automatically, and whatever remains is carved into labeled “envelopes” that mirror real life—groceries, fuel, streaming, co-pays, pet supplies. Each category holds a hard ceiling; when the allocated cash or digital balance hits zero, the category is closed until the next income cycle. The tactic originated during the Great Depression when banks folded and families dealt only in cash, but the same psychological guardrails still work in an era of contactless payments and same-day delivery. Behavioral economists call the approach “pre-commitment with salient feedback”: the physical or digital pile shrinks in real time, forcing the brain to register opportunity cost with every swipe or bill peeled away.The system accommodates both tactile and tech-forward households. Purists withdraw the full discretionary sum on payday, sort it into color-coded envelopes stored in a fire-safe box, and carry only the day’s relevant envelope. Digital adopters move the identical amounts to sub-accounts inside an online bank or to category wallets inside apps such as Goodbudget, YNAB, or Qube Money; the money stays FDIC-insured and can earn 4–5 % annual interest if parked in a high-yield savings bucket. Hybrid users mix tactics—groceries and restaurants in cash to curb impulse chips, gas and travel in a card-linked app to capture roadside rewards. Whichever path you choose, the discipline remains identical: money is spent only from its designated envelope, turning abstract budget lines into concrete, exhaustible resources.Core Mechanics and Monthly Setup RoutineSetting up the system takes roughly 45 minutes once you have three months of prior spending data. First, list every variable category that isn’t on autopilot; omit mortgage, insurance, and loan payments because those are fixed and non-negotiable. Second, average the last three months in each bucket, then shave or boost the figure to match current goals—perhaps trim take-out from $280 to $200 and add the $80 savings to a sinking fund for holiday flights. Third, sum all envelopes; if the total exceeds leftover income, keep shaving until the math is zero-based. Fourth, decide the medium: paper, digital, or hybrid. Fifth, on payday, fund each envelope immediately—lag time breeds “invisible” discretionary cash that evaporates on impulse buys. Finally, receipt-drop every transaction into the tracking app or notebook the same day; missing even two entries can throw off the month-end reconciliation.Converting direct-deposit income into physical cash demands a small security protocol. Withdraw inside the bank lobby, not the outdoor ATM, and request mixed bills—twenties for groceries, tens for pharmacy runs, fives for coffee—so you’re not forced to break large denominations in the store. At home, store envelopes in a fireproof bag or safe; never label the outside with the total, only the category, to reduce theft temptation. When you shop, carry just the envelope you need plus a backup $10 in your wallet; leaving the rest at home prevents “rob Peter” raids between categories. For couples, each partner takes a photo of the funded envelopes and initials a shared ledger; that simple audit step prevents the “I thought we had more” arguments that derail many starter budgets.Advantages That Strengthen Cash-Flow DisciplineEnvelope budgeting delivers five concrete advantages over mental budgeting or retroactive spreadsheet tracking. First, visibility: watching a stack dwindle to two twenties creates an immediate, emotional speed bump that a declining bank-pixel number rarely achieves. Second, built-in fraud protection: if a purse or envelope is lost, the damage is capped at that category’s balance, not the entire checking account. Third, interest avoidance: consumers who finish the month with surplus groceries or fuel money can sweep the excess to high-yield savings the same evening, earning roughly 0.33 % monthly (4 % annualized) instead of letting it sit idle at 0.02 % in a basic checking product. Fourth, couple alignment: partners can literally hand off the “dining out” envelope mid-month, making the remaining balance a neutral third party in spend-or-save debates. Fifth, credit-score rehabilitation: by capping discretionary swipes, users report 17–23 % lower utilization ratios within six months, a figure credit-bureau simulations translate to a 15- to 30-point score lift for cardholders previously stuck above the 30 % threshold.Academic research supports the anecdotal hype. A 2022 Journal of Consumer Affairs study followed 412 low-to-moderate income households; those assigned to envelope-style partitioned accounts reduced grocery waste by 12 % and cut impulse clothing purchases by $47 per month compared with the control group using conventional ledgers. Over a calendar year, the average envelope family accumulated $564 in unanticipated savings—money that was redirected to emergency funds, shaving nearly three weeks off their hypothetical unemployment runway.Drawbacks and Real-World Friction PointsDespite its strengths, the method can clatter against modern commerce. Ride-share, mobile tolls, and subscription upgrades all require a card on file; if the “transportation” envelope is physical, you must manually move cash back to the bank before the charge posts, negating some of the psychological guardrails. Cash loss remains an immutable risk: homeowners insurance typically reimburses a maximum of $200 in currency, far below a monthly grocery envelope. Partner coordination grows complex when one spouse travels for work and needs remote envelope access, yet joint fintech wallets still lack real-time parental controls that prevent accidental overspending from a shared bucket.Interest forfeiture is another subtle cost. Parking $1,500 in paper for a full month instead of a 4 % annual savings account sacrifices about $5 in interest each cycle—modest, yet $60 a year can fund an annual IRA contribution for a young saver. Finally, cash-only households forfeit card rewards; a 3 % grocery card returning $21 on $700 of spending effectively raises your envelope budget by that amount, so strict envelope adherents need to re-evaluate the trade-off quarterly.Hybrid and Digital Variations for 2026Fintech companies have cloned the envelope philosophy inside insured, card-based wrappers. Qube Money, for instance, opens a master checking account and up to 50 “qubes”; swipes are approved only if the user pre-selects a category in the app, replicating the tactile “choose an envelope” moment at the register. YNAB’s digital age-of-money algorithm sweeps unused dollars into next month’s envelopes automatically, smoothing income fluctuations for gig workers. Some regional credit unions now offer “envelope savings pods” that pay 5 % on balances up to $1,000 per pod, effectively turning last month’s surplus grocery money into a high-yield micro-CD.For households uncomfortable with neo-banks, mainstream institutions such as Ally and Capital One 360 allow free sub-accounts nicknamed for envelopes; users can maintain up to thirty buckets and schedule automatic transfers on payday. Pairing those accounts with a no-fee rewards debit card keeps the system entirely inside FDIC-insured walls while still producing merchant-category email alerts that function like digital receipts.Action Steps to Launch Your First Envelope CyclePrint or export the last 90 days of checking-account activity; highlight every discretionary swipe in yellow. Cluster the yellow lines into 6–10 realistic envelopes; resist micro-categories such “snacks” or “coffee” unless those line items consistently exceed $40 a month. Reduce the summed average by 5 % to create a slim surplus cushion; if income is unstable, reduce by 10 %. Open a no-fee high-yield savings account and nickname it “Envelope Surplus Reservoir”; this is where unspent money earns interest until next month’s refill. Decide cash vs. digital; if cash, schedule an in-branch withdrawal for mixed bills the same morning your paycheck clears. Snap a photo of each funded envelope and store it in a shared cloud folder visible to all adult household members. Commit to a mid-month 10-minute huddle to compare envelope balances against calendar obligations—birthday dinners, field-trip fees, oil changes—so no category blindsides you in the final week.In Dayton, Ohio, for instance, newlywed teachers Emily and Luis Rojas found that swapping from a shared debit card to color-coded paper envelopes cut their post-wedding Target splurges from $180 a month to $92 within two cycles; the $88 monthly difference now funds a vacation sub-account already holding $616 after seven months.Critics argue the system feels regressive in an age of payments, yet the move raises questions about whether convenience or control matters more to household balance sheets. Unexpectedly, Gen-Z users on TikTok have revived the hashtag #CashStuffing, posting weekly “envelope stuffing” videos that rack up millions of views—proof that tactile budgeting still carries social currency.Useful ResourcesGoodbudget – App that syncs digital envelopes across household phones and exports spending reports to Excel. Qube Money – Debit-card envelope system that requires pre-selection of a category before each purchase. FDIC Consumer News “Managing a Money System” – Free PDF leaflet outlining security tips for cash and digital sub-accounts. YNAB YouTube Channel – Library of 5-minute tutorials on zero-based, envelope-style budgeting for variable incomes.Sources: Journal of Consumer Affairs 2022 study; FDIC Consumer News; developer documentation from Goodbudget, Qube Money, YNAB.

Budget Management and Cash Flow

Budget Management and Cash FlowHow Much to Save Each Month: Budget Rules for 2026

Only 41 percent of U.S. adults can pay a surprise $1,000 bill from savings, Bankrate’s 2025 Emergency Savings Report shows. That stark figure underscores why setting a monthly savings target—however modest—remains the first concrete move toward breaking the paycheck-to-paycheck cycle. Why the 15–20% Rule Still Dominates Advice Certified financial planners have long preached the gospel of siphoning off 15–20 percent of gross income before living expenses even register. The range is not arbitrary: it captures the average amount needed to fund a 30-year retirement at 80 percent of pre-retirement income while simultaneously building a liquidity cushion. Laura Davis, CFP and founder of Financial Labs Inc., cautions that the ratio “works best for households with stable wages and employer retirement matches already baked in.” Translation—if your 401(k) receives a 4 percent company match, only 11 percent more is required from your own pocket to land inside the band. The figure also folds in health-savings-account deposits, 529 college contributions, and extra mortgage principal, not just idle cash in the bank. How the 50/30/20 Budget Handles Savings For savers who think in percentages of take-home pay, the 50/30/20 rule offers a lighter mental lift. Half of net income covers needs—rent, utilities, insurance minimums—while 30 percent funds discretionary wants. The remaining 20 percent is earmarked for “financial priorities,” a bucket that blends saving and debt payoff. A household clearing $4,500 after taxes would therefore route $900 a month toward Roth IRA deposits, emergency-fund transfers, and additional student-loan principal. Behavioral economists like the rule because it forces trade-offs inside each silo; overspending on restaurants cannot leak into rent money, and the 20 percent floor keeps savings on autopilot even when income rises. Tailoring the Percentage to Your Income Tier Low-income families often confront a mismatch between fixed costs and earnings; rent alone can exceed 40 percent of gross pay. Advisors recommend an initial savings rate of 5–10 percent directed solely into a starter emergency fund—usually one month of core expenses—held in a high-yield online account currently paying 4–5 percent APY. Middle-income earners—roughly $55,000–$120,000 for a dual-income household—can ratchet the rate toward 15 percent once high-interest credit cards are tamed. High earners face the opposite risk: lifestyle creep. Pushing the savings rate above 20 percent captures additional tax-deferred space—think 403(b) and mega-backdoor Roth strategies—while insulating portfolios from sequence-of-returns risk decades before retirement. Where to Park the Cash for Maximum Growth Account selection matters as much as the dollar amount. Emergency reserves belong in FDIC-insured high-yield savings or money-market accounts where daily liquidity is guaranteed and interest compounds daily. Goal-specific money needed within three years—say, a car replacement—can tolerate a short-term Treasury ETF sporting slightly higher volatility but negligible credit risk. Retirement dollars should ride equity index funds inside tax-favored wrappers; a 25-year-old earning 7 percent real returns turns $500 monthly into roughly $790,000 by age 60, compared with $290,000 in a 0.5 percent savings account. Health savings accounts, often overlooked, offer triple tax advantage and can double as stealth retirement vehicles after the emergency benchmark is met. Rebalancing Your Rate as Life Evolves Savings targets are not static. Marriage, home purchases, or a shift to freelance income should trigger a fresh calculation. A simple annual audit—add up all household cash-flow surpluses, divide by gross income, compare with the prior year—keeps the percentage honest. Automate escalation: schedule 1 percent increases every six months until the ceiling feels tight, then pause. Finally, redirect windfalls—bonuses, tax refunds, restricted-stock vests—before they reach checking accounts; behavioral research shows once money is labeled “spendable,” the psychological hurdle to move it skyrockets. Emergency-Fund Benchmarks by Life Stage Critics argue the classic “three-to-six months of expenses” mantra glosses over real-world volatility. In practice, single renters with robust health coverage can land on the lower end, while dual-income parents with a mortgage and childcare bills often stockpile nine months. Unexpectedly, the rise of gig work nudges the target higher still; freelancers in Austin, for instance, report saving 12 months of overhead after 2023’s tech-contract freeze. Automation Tools to Keep You Honest Fintech apps such as Qapital and Ally Bank’s Surprise Savings algorithm sweep micro-amounts into sub-accounts every few days, trimming the temptation to spend. Meanwhile, employer payroll portals increasingly allow split deposits across four or more institutions, letting workers siphon retirement, emergency, and vacation funds before the net paycheck even lands. Tax-Sheltered Options Beyond the 401(k) Once the emergency fund is flush, extra cash can flow into a Roth IRA (2026 limit: $7,000 under 50) or, for high-deductible health plans, an HSA (contribution cap: $4,150 individual, $8,300 family). Both vehicles grow tax-free, and the HSA allows penalty-free withdrawals for any purpose after age 65, making it an unexpectedly flexible pot of money. Useful Resources Bankrate 2025 Emergency Savings Report – Full survey data on American saving habits and breakdowns by age and region NerdWallet 50/30/20 Calculator – Interactive spreadsheet that auto-splits net income into the three buckets and graphs progress TreasuryDirect.gov – Purchase 4-, 8-, 13-, or 26-week Treasury bills online with no brokerage fees for short-term surpluses Vanguard Roth IRA Starter Kit – Step-by-step guide to opening, funding, and selecting low-cost index funds within IRS limits

Budget Management and Cash Flow

Budget Management and Cash Flow50/30/20 Budget Rule: Simple Guide to Split Needs, Wants, Savings

The 50/30/20 Budget Rule: A Simple Framework for Managing Cash Flow and Building Savings The 50/30/20 budget rule offers a straightforward alternative to complex spreadsheets and category-heavy spending plans. By dividing after-tax income into three broad buckets—50% for needs, 30% for wants, and 20% for savings and debt repayment—this method helps households stabilize cash flow without micromanaging every purchase. The appeal is obvious: instead of tracking 47 micro-categories, you guard three wide lanes and let daily trade-offs happen inside each lane. How the 50/30/20 Formula Works in Practice Start with your net take-home pay: the amount that actually hits your checking account after federal, state, and payroll taxes are removed. Ignore pre-tax deductions such as health-insurance premiums or transit benefits for now; those will be slotted into one of the three buckets later. Multiply the net figure by 0.50, 0.30, and 0.20 to arrive at dollar ceilings for each tier. A nurse earning $5,400 after tax, for example, would aim for $2,700 in needs, $1,620 in wants, and $1,080 in savings or extra debt payments. The beauty lies in the absence of sub-limits. Once the $1,620 “wants” allowance is set, the user can blow it all on a weekend trip or spread it across streaming subscriptions, restaurant outings, and a new phone—no guilt, no re-tabulation. The same freedom applies inside the 50% needs corridor: rent, utilities, groceries, car payments, and the minimum on student loans all compete for the same pooled amount, forcing the user to decide what matters most rather than what fits a micro-category. In other words, the rule hands you guardrails, then lets you steer. Defining Needs, Wants, and Savings Contributions Needs encompass anything that protects health, safety, income, and credit score. Housing costs—rent, mortgage principal, interest, insurance, and condo fees—land here, as do basic utilities (electricity, water, heating fuel), groceries, required childcare, fuel or transit passes, and minimum loan installments. Gym memberships, meal-delivery kits, or a second car, however, slide into wants unless you can document that losing them would endanger employment or safety. Critics argue the boundary can blur: a smartphone is clearly a want until you drive for a ride-share app after your day job, at which point it jumps the fence. Wants are upgrades or add-ons: restaurant meals, premium cable, boutique fitness, vacation flights, designer clothing, hobby gear, gifts, and the latte factor. A quick test is to ask whether you could survive four weeks without the item while still working and eating. If the answer is yes, it is discretionary. Unexpectedly, pet-care costs often straddle the fence; a goldfish is a want, but a service animal that keeps a diabetic owner safe is a need. When in doubt, place the item in whichever bucket feels tighter that month; the exercise alone clarifies priorities. The 20% savings/debt slice is the wealth-building corridor. Extra principal payments on credit-card balances, private student loans, or auto notes fall here, as do contributions to emergency funds, Roth IRAs, 401(k)s, brokerage accounts, and sinking funds for a home down payment or wedding. Minimum loan payments remain inside needs; anything above the required amount shifts to this tier, immediately boosting net worth or cutting total interest. In Miami, for instance, one public-school teacher paid an extra $350 toward her 9% car note every month; the move shaved 14 months off the term and saved $1,140 in interest, all from the 20% slice. Common Pitfalls and How Households Trip Up New adopters routinely underestimate how much of their income is already locked into fixed obligations. A 2025 Bureau of Labor Statistics survey shows the median renter in a coastal metro now allocates 38% of net pay to rent alone; once utilities, groceries, and a basic phone plan are layered in, the 50% threshold is blown before the car note appears. In that scenario, the rule still functions, but the percentages flex—perhaps 58/22/20—until a lease can be renegotiated, a roommate added, or income raised. The key is to write the real numbers down; pretending rent is 28% when it is 38% only delays the fix. The second trap is lifestyle creep inside the wants corridor. Because no line item is forbidden, users can rationalize almost anything as a “want” and burn through the 30% weeks before the month ends. Behavioral-finance researchers at the University of Chicago found that households using ratio budgets spend 11% more on discretionary items in the first six months than those using zero-line budgets, precisely because psychological accounting is looser. Automating the 20% transfer on payday—before discretionary spending starts—counteracts the drift. Separately, deleting stored credit-card numbers from retail sites adds friction that slows impulse buys. Finally, the 20% savings slice can feel abstract when high-interest debt lingers. Financial planners usually recommend stashing at least one month of core expenses ($1,000–$2,000) in a high-yield savings account as a firewall, then deploying the full 20% toward debt with rates above 7%. Once the balance is cleared, the same cash flow accelerates long-term savings, effectively moving households from 58/22/20 to a wealth-building 50/30/20 within two to three years. Skipping the emergency step, however, invites the next surprise bill to reappear as a fresh credit-card balance, wiping out hard-won progress. Adapting the Rule for Irregular Income Freelancers, seasonal workers, and commission-based employees can still use the framework, but the calculation flips to annual rather than monthly dollars. Total last year’s net income from all 1099s and W-2s, divide by 12 to obtain a normalized monthly figure, then apply the 50/30/20 split. Hold the 20% in a separate high-yield account each time a payment arrives; sweep the surplus into needs and wants only after quarterly taxes are set aside. During above-average months, the surplus stays parked in the savings bucket, automatically cushioning lean periods without forcing a budget rewrite. Meanwhile, during below-average months, draw from the same bucket to keep needs fully funded; the percentages stay intact on an annual view even if they wobble month to month. In related developments, some gig drivers now treat each direct deposit as a mini-payroll: 20% off the top slides into a “do-not-touch” sub-account at Ally or Marcus, 30% lands in a “fun debit card,” and the remainder covers gas, car insurance, and rent. The physical separation, they say, removes the mental math that once led to accidentally spending next month’s rent on late-night tacos. Tech Tools That Do the Math for You Manual spreadsheets work, yet most users last longer when the sorting is invisible. Quicken Simplifi, Monarch Money, and You Need a Budget (YNAB) all allow custom category groups labeled Needs, Wants, and Savings. After a one-time setup, transactions auto-import from linked checking, credit-card, and investment accounts; the dashboard flashes green when each bucket is under its monthly ceiling and red when projected to overspend. For spreadsheet loyalists, Tiller Money feeds bank data into Google Sheets templates that already embed the 50/30/20 formulas—no coding required. Meanwhile, Mint loyalists who migrated to Credit Karma after Mint’s 2024 shutdown can still export last year’s CSV and run a quick pivot table to benchmark the first annual split. Real-World Benchmarks to Gauge Progress By age 30, aim for the savings/debt corridor—plus any employer 401(k) match—to represent at least 25% of gross income, even if the 50/30/20 rule is still calibrated on net pay. By 40, the cumulative savings bucket should exceed one year’s gross salary, according to Fidelity’s 2025 retirement roadmap. If those mileposts feel distant, raise the 20% to 22% every time you receive a cost-of-living raise; the adjustment is barely noticeable day-to-day yet compounds to an extra $70,000–$90,000 over a thirty-year career at median income levels. In dollar terms, a worker earning $65,000 who bumps the savings slice from 20% to 22% nets an additional $1,300 per year; invested at a 7% annual return, that single tweak grows to roughly $88,000 by retirement. When to Choose a Different Framework The 50/30/20 rule loses efficiency once nondiscretionary costs fall meaningfully below 50%. High earners living in low-cost areas, for instance, may find needs consuming only 30% of net pay; forcing 30% into wants invites gratuitous spending. Those households often pivot to a 30/20/50 model—30% needs, 20% wants, 50% savings—or adopt the “pay-yourself-first” method, treating every incoming dollar as a 401(k) or brokerage contribution until the annual IRS limit is reached, then spending what remains. Physician families in Texas, for example, sometimes max out two 401(k)s, two 457(b)s, and a cash-balance pension—north of $90,000 in 2026—before they even consider the wants bucket, a sequence that can propel them to financial independence two full decades ahead of schedule. Conversely, households trapped in 70% needs territory—common for single parents carrying student loans—should not abandon structure altogether. A temporary 70/15/15 split still captures the behavioral discipline of targeted savings, even if the timeline for debt freedom stretches longer. The key is to revisit the percentages every six months; each paid-off loan or slight income bump reclaims bandwidth for the 20% corridor. Over time, the goal is to migrate back toward 50/30/20, not to abandon budgeting entirely. Useful Resources Consumer Financial Protection Bureau Budget Worksheet – Free PDF that pre-labels needs, wants, and savings lines to speed your first 50/30/20 audit. NerdWallet Debt Payoff Calculator – Run “avalanche vs. snowball” scenarios to see how the 20% slice can wipe out high-interest balances fastest. IRS Paycheck Estimator – Plug gross wages and withholding allowances to pinpoint the exact net income figure your budget should use. Fidelity Retirement Score Quiz – Translate current savings rates into projected retirement income so you know whether 20% is sufficient—or needs an upgrade. Sources: Bureau of Labor Statistics 2025 Consumer Expenditure Survey; Fidelity Investments Retirement Roadmap 2025; University of Chicago Booth School behavioral-finance working paper, February 2026.

Budget Management and Cash Flow

Budget Management and Cash FlowHow Inflation Erodes Savings and Cash Flow: 2026 Protection Tips

U.S. inflation measured 3.5 % for the 12 months ending March 2024, still one-and-a-half percentage points above the Federal Reserve’s 2 % goal. That gap quietly drains household budgets and silently shrinks the real value of money already set aside for emergencies, college, or retirement. Critics argue the headline number masks bigger swings in rent, eggs, and car insurance—categories where bills arrive every 30 days, not once a quarter. How 3.5 % Inflation Quietly Cuts Buying Power A 3.5 % annual pace may sound mild compared with the four-decade peak of 9.1 % touched in June 2022, yet the math compounds quickly. A basket that cost $100 last March now costs $103.50; stretch the same rhythm over three years and the tab edges toward $111. Fetching the identical cart of groceries therefore demands either an 11 % larger income balance or an 11 % sacrifice somewhere else. Wage growth, currently near 4.2 % in private-sector data, is barely outpacing the price index, leaving little margin for new saving. Economists label this phenomenon “static real income”: paychecks rise, but living standards stay flat because the purchasing power of every dollar recedes. In Phoenix, for instance, one school-district accountant told researchers her 3.8 % COLA “felt like a freeze” once rent jumped 6 %. Traditional Savings Accounts Surrender Value Daily Cash kept in classic savings vehicles loses ground each statement cycle. The national average annual percentage yield (APY) on standard savings remains stuck at 0.47 %, according to FDIC figures updated March 2026. A $10,000 deposit therefore earns $47 over a full year, yet at 3.5 % inflation the same pile needs to grow $350 just to retain its original buying power. The shortfall—$303 after twelve months—illustrates “real negative return,” a situation in which nominal balances climb while inflation-adjusted wealth falls. Certificates of deposit (CDs) fare only marginally better: the average 12-month CD yields 1.6 %, translating to a real loss of roughly 1.9 % once price erosion is factored in. Consumers who rely on these instruments for safety end up financing that safety through gradual wealth decay. The move raises questions about whether “risk-free” and “return-free” have become synonyms. Rising Prices Push Emergency Funds Into Debt Territory Higher prices do not merely shave existing balances; they also reduce the surplus cash households can divert toward future goals. Bureau of Labor Statistics outlays show that average weekly spending on essentials—food, fuel, utilities, insurance—has climbed 17 % since 2021, adding roughly $170 to the typical household’s monthly nut. When costs accelerate faster than take-home pay, families confront an unappealing triage: trim discretionary categories, tap credit cards, or throttle the automatic transfer meant for rainy-day reserves. Survey data from the Consumer Financial Protection Bureau released February 2026 found 38 % of adults had decreased their savings contribution at least once in the prior six months specifically “because everyday expenses grew.” Smaller inflows, layered onto negative real returns, can evaporate a once-solid emergency cushion within a year. Financial planners now recommend restocking the fund whenever cost-of-living adjustments (COLAs) lift wages, treating the raise as mandatory replenishment rather than spendable income. Separately, credit-union managers report a 22 % spike in small-dollar personal loans drawn against depleted savings, a pattern last seen in 2009. Strategic Vehicles That Outrun the CPI Escaping the erosion cycle requires pairing higher nominal yields with instruments that reset or float alongside policy rates. High-yield online savings accounts, many offered by federally-insured banks with low overhead, currently advertise APYs of 5.05 % to 5.30 %—enough to deliver a slim but positive real return after inflation and ordinary taxes. Another layer of protection is laddered CDs: by purchasing sequential six-, 12-, and 18-month certificates, savers capture elevated short-term rates while preserving quarterly liquidity. Series I savings bonds issued by the U.S. Treasury go a step further; their composite rate combines a fixed component (0.4 % for bonds sold through April 2026) with a variable piece tied to headline CPI, guaranteeing that the investment at least paces inflation for up to 30 years. Purchase limits ($10,000 per Social Security number online) make them a satellite rather than a core holding, yet they remain the closest thing to a CPI-linked sleep-well asset available to retail investors. Meanwhile, unexpectedly strong tax-refund season has pushed some filers to park the entire rebate in I-bonds before the May reset. The Case for Investing Surplus Cash Long-Term Money not needed within three to five years historically benefits from equity-market participation. Since 1950 the S&P 500 has returned about 10.1 % annually including dividends, dwarfing the 3.7 % average inflation rate over the same span. Volatility is real—2022 delivered an 18 % drawdown right when inflation spiked—but broad index exposure held for five-year rolling periods has beaten CPI in more than 84 % of observed windows. Dollar-cost averaging, the practice of investing equal amounts at regular intervals, smooths entry prices and counters the behavioral urge to “time” cyclical bottoms. Target-date retirement funds or globally diversified exchange-traded funds (ETFs) allow low-maintenance participation without single-stock risk. The key discipline is segregating liquidity buckets: keep near-term obligations in insured cash vehicles yielding at least 4 %, while directing longer-term surplus toward growth assets expected to out-earn inflation over a decade or more. Critics argue the next decade’s return could undershoot if valuations stay elevated, yet even a 7 % nominal beat would handily clear today’s 3.5 % price hurdle. Budget Tactics That Restore Contribution Room Recapturing contribution capacity starts with line-item auditing rather than vague belt-tightening. Begin by downloading three months of bank and card statements into a spreadsheet, then tag every transaction with a category and a “utility score” of 1 to 3, where 1 equals “bare necessity” and 3 equals “nice but forgettable.” Research from the University of Chicago’s Booth School shows consumers who score spending this way trim an average 11 % from discretionary outflows without perceiving a lifestyle drop. Redirect the first month’s savings into the high-yield emergency fund; thereafter, automate transfers on payday so the money exits checking before discretionary temptities surface. Another tactic is subscription triage: streaming, cloud storage, and app bundles renew silently; canceling or downgrading just four services typically frees $40–$60 monthly—enough to max an IRA contribution for many middle-income filers. Finally, negotiate fixed bills. Insurance carriers often match competitor quotes if a customer phones ahead of renewal; internet providers frequently offer $20 loyalty discounts that can be stacked with autopay credits. These micro-moves cumulatively reopen the cash funnel that inflation tried to close. Policy Outlook: Why Inflation Could Linger Near 3 % Fed officials have signaled only two quarter-point rate cuts for 2026, fewer than markets expected last winter, citing sticky services inflation and tight labor supply. Housing costs—one-third of CPI—remain buoyant because multi-family construction starts slowed after 2023’s regional-bank credit crunch. Energy markets offer little relief; geopolitical tension in the Red Sea and maintenance backlogs on Gulf Coast refineries keep Brent crude above $80 per barrel, feeding directly into gasoline and core goods prices. Taken together, consensus forecasts published by the Philadelphia Fed place headline inflation at 2.8 % by December 2026, still above target. Savers should therefore plan for another 18–24 months of elevated cost pressure, reinforcing the importance of yield-bearing, CPI-linked, or growth-oriented vehicles rather than low-interest cash drag. Meanwhile, Congress is debating a bill that would raise the I-bond purchase cap to $15,000, a change that could pass late summer if budget scoring remains favorable. Action Steps Open an FDIC-insured high-yield savings account yielding ≥4.5 % and migrate at least one month of living expenses there this week. Purchase a 6-month CD with surplus funds you will not need before autumn; roll proceeds into a 12-month certificate at maturity to lock the rate curve. Log onto TreasuryDirect and buy $5,000 in Series I bonds before May 1, 2026, to secure today’s 0.4 % fixed component plus CPI adjustment. Increase your 401(k) or IRA contribution by 1 % of salary; the pre-tax shield effectively boosts the real return compared with taxable cash. Schedule quarterly budget reviews on your calendar for the next 12 months; automate reminders to renegotiate streaming, insurance, and telecom bills each cycle. Sources: U.S. Bureau of Labor Statistics, Federal Deposit Insurance Corporation, U.S. Treasury, Federal Reserve Bank of Philadelphia, Consumer Financial Protection Bureau, University of Chicago Booth School of Business.

Budget Management and Cash Flow

Budget Management and Cash Flow15/65/20 Budget System: How to Allocate Every Dollar for Long-Term Cash Flow

High earners hire tax attorneys, portfolio strategists, and family-office CPAs, yet the scaffolding that keeps their balance sheets intact is neither trademarked nor encrypted.A three-bucket formula—15 % to future wealth, 65 % to daily operating costs, 20 % to fun—can be copied by anyone with a checking account and a calendar alert. 15/65/20 Formula Breakdown for Monthly Budgeting The rule splices take-home pay into defensive, overhead, and lifestyle layers.Fifteen cents of every after-tax dollar exit the spending economy the moment the deposit lands: automatic transfer to a high-yield savings account, Roth IRA, or zero-fee index fund.Sixty-five cents cover the non-negotiables that keep life running—rent, utilities, insurance, groceries, commuting, minimum debt service.The final twenty cents are guilt-free; streaming subscriptions, weekend trips, or artisan coffee remain permissible so long as the plastic swipe stays inside this fenced pasture.Because the sequence is fixed—save first, spend last—the system prevents the human tendency to raid leftovers that never materialize. Origins of the 15/65/20 Budget Method Senator Elizabeth Warren’s 50/30/20 blueprint popularized percentage-based budgeting in 2005, but wealth managers noticed a flaw among six-figure clients: thirty percent for wants invited lifestyle creep.By collapsing wants to twenty and hiking essentials to sixty-five, advisors created a steeper tilt toward investments without forcing renters to live on rice and beans.The tweak also acknowledges today’s cost structure; healthcare premiums, phone plans, and daycare prices that did not exist in earlier decades now sit inside the “essential” tent.Warren Buffett’s dictum—“spend what is left after saving”—is baked into the first line of the spreadsheet, turning a slogan into an ACH transfer. How High Earners Still Miss the Mark PYMNTS surveyed 4,000 U.S. households in 2023 and discovered that thirty-two percent of those earning above $200,000 live paycheck-to-paycheck; the culprit is mortgage-for-household-ratio above 40 % and recurring subscriptions that exceed $1,100 a month.Wealth managers tell of clients who max out 401(k)s yet finance $90,000 SUVs at 7 % APR, illustrating that high income without a guardrail simply raises the speed limit for overspending.The 65 % ceiling acts as an internal credit underwriter, denying permission for fixed costs to mushroom, even when a lender pre-approves a larger note. Cutting Core Costs Without Deprivation Bureau of Labor Statistics 2024 data show the median U.S. household lays out 34 % of income on housing, 17 % on transportation, and 13 % on food—collectively the fat target inside the 65 % lane.House-hackers rent out basements on Airbnb, turning liability into cash flow; car-buyers purchase three-year-old off-lease vehicles whose depreciation curve has already snapped downward; meal-planners adopt “protein first” grocery lists that curb impulse snack spending.Each percentage point shaved from these big-three categories translates into $500-$700 of annual breathing room on a $75,000 salary, money that can be rerouted to the 15 % wealth bucket with no income lift required.In Austin, Texas, for instance, a couple trimmed their housing share from 36 % to 28 % by accepting a roommate for twelve months; the $6,200 saved financed the husband’s AWS cloud certificate, which later lifted his salary 18 %. Automating the 20 % Lifestyle Bucket Behavior-finance studies reveal that labeled accounts reduce spending by 10-15 % versus a generic checking balance.Create a separate “Fun” debit card capped at 20 % of net pay; when the envelope is empty, the card declines, protecting the other 80 % from raids.Couples report fewer money arguments because permission is preset; one partner’s concert tickets never morph into a referendum on shared priorities.Any unspent portion rolls into next month, letting savers pre-fund larger indulgences such as international travel without tapping emergency reserves.Critics argue the 20 % cap still rewards conspicuous consumption, yet defenders counter that a sanctioned outlet prevents the binges that blow budgets to pieces. Action Steps Log last three months of take-home pay and sort transactions into savings, essential, discretionary. Open a high-yield online savings account and schedule an automatic 15 % transfer for the day after each paycheck. List fixed essentials; target 65 % by renegotiating insurance, refinancing high-rate debt, or finding a roommate. Create a “Fun” checking account with its own debit card and cap deposits at 20 % of income. Re-audit percentages every quarter; raises go 75 % to the 15 % bucket, 25 % to discretionary until the emergency fund covers nine months. Sources: PYMNTS 2023 survey; Bureau of Labor Statistics 2024 Consumer Expenditure Report; Federal Reserve Board Survey of Consumer Finances